Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

Manchin’s ‘Inflation Reduction Act’ One Giant, Misnamed Nothingburger, Goldman Finds: “It Will Change Fiscal Impulse By Less Than 0.1% Of GDP”

While few have had a chance to read the details of the Manchin-Schumer so-called “Inflation Reduction Act” (where the only inflation reduction is in the title and nowhere else) especially those who have been championing it all day across various media outlets, Goldman’s chief political economist Alec Phillips spent the night digging into the nuances of the proposed bill and found … well… nothing.

As Phillips writes, the fiscal deal that already looked likely to pass now looks likely to be a bit broader than expected: the potential Senate deal now includes a version of the corporate minimum tax the House passed late last year, as well as a package of energy provisions similar in size to the House-passed bill. However, and this is the punchline, the Goldman strategist finds that “the fiscal impact remains limited” and warns that “over the next few years, it looks unlikely that this bill would change the fiscal impulse by more than 0.1% of GDP, as new spending and new taxes roughly offset and, in any case, both are fairly small in absolute terms.”

Goldman concludes that while the details are still apt to change – the tax increase might shrink even more – this version of the bill looks fairly likely to become law, although “the omission of any changes to state and local tax deductibility raises some questions about House passage.”

Below we excerpt from the Goldman note (the full pdf available to pro subscribers)

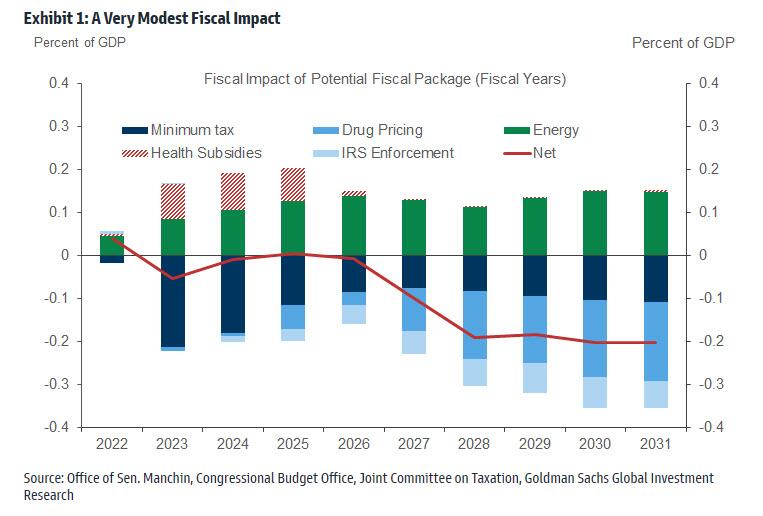

The fiscal deal that looked increasingly likely now also looks a bit broader than expected. In a surprising turn of events, Senate Majority Leader Schumer (D-N.Y.) announced an agreement (summary here, text here) with Senator Manchin (D-W. Va.) on a somewhat broader fiscal package than we and most others had expected. Instead of limiting the package to Medicare drug pricing changes ($288bn/10yrs in savings) and two year extension of health insurance subsidies ($22bn/yr), the deal also includes $369bn/10yrs in energy and climate incentives and one additional year of health insurance subsidies, funded by a 15% minimum tax on corporate book income for companies with more than $100 million in domestic income/$1 billion in global income (raises $313bn/10yrs in tax revenue), and extending the minimum holding period for taxation of carried income at the long-term capital gains rate to 5 years from the time a fund acquired substantially all of its investments ($14bn/10yrs). In both cases, the tax increases would take effect from 2023.

The net fiscal impact of these policies looks likely to be very modest, likely less than 0.1% of GDP for the next several years. Exhibit 1 provides a rough estimate, based on the cost estimates of the Senate drug pricing language released a few weeks ago, and estimates of the relevant tax provisions and energy provisions from the House-passed bill. While the final outcome is likely to differ in details from those provisions, the fiscal impact is likely to be similar.

The bill is called the “Inflation Reduction Act of 2022” but the individual provisions it includes appear to be substantially the same as prior bills. In theory, the drug pricing provisions could impact the prices that Medicare-eligible consumers pay for drugs, but those changes would not take effect until 2026. Likewise, the renewable energy provisions are unlikely to have a near-term impact on energy–and in particular, gasoline–prices and are instead focused on medium term investment and production. We note that while the summary from Sen. Manchin’s office mentions energy permitting changes, it is unclear whether this “reconciliation” bill could include such regulatory changes, as those are generally precluded by Senate rules prohibiting non-fiscal matters from inclusion in reconciliation legislation.

The legislation will probably still change. It seems likely that there will be some additional changes on the tax side. It is unclear whether the carried interest tax changes will pass as written, and there is a fair chance they could still be removed from the bill before passage. Additional carve-outs to the minimum tax proposal look likely, as various constituencies try to preserve the ability of corporations to take advantage of specific tax deductions and credits when companies pay the minimum tax.

Passage looks likely, but not guaranteed. It is not yet clear whether virtually every Democrat, whose support will be needed to pass the bill in the House and Senate, will be willing to vote for this agreement. Our expectation is that they will, but there are still obstacles. The most obvious is the omission of any expansion of the state and local tax deduction, which some House Democrats have insisted be included in return for their support.

More in the full note available to pro subscribers in the usual place.

Tyler Durden

Thu, 07/28/2022 – 14:41

Continue reading at ZeroHedge.com, Click Here.