Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

Carnage: China Breaks, Apple Cracks Key Support, Yields Soar As Rate Hike Odds Surge

The week started off badly enough with nothing short of epic devastation in China, as stocks listed in Hong Kong had their worst day since the global financial crisis amid concerns over Beijing’s close relationship with Russia, a surge in covid cases leading to a lockdown in Shenzhen, and renewed regulatory risks all of which sparked panic selling.

The Hang Seng index dropped more than 4%, sliding below 20,000 to the lowest level since 2015…

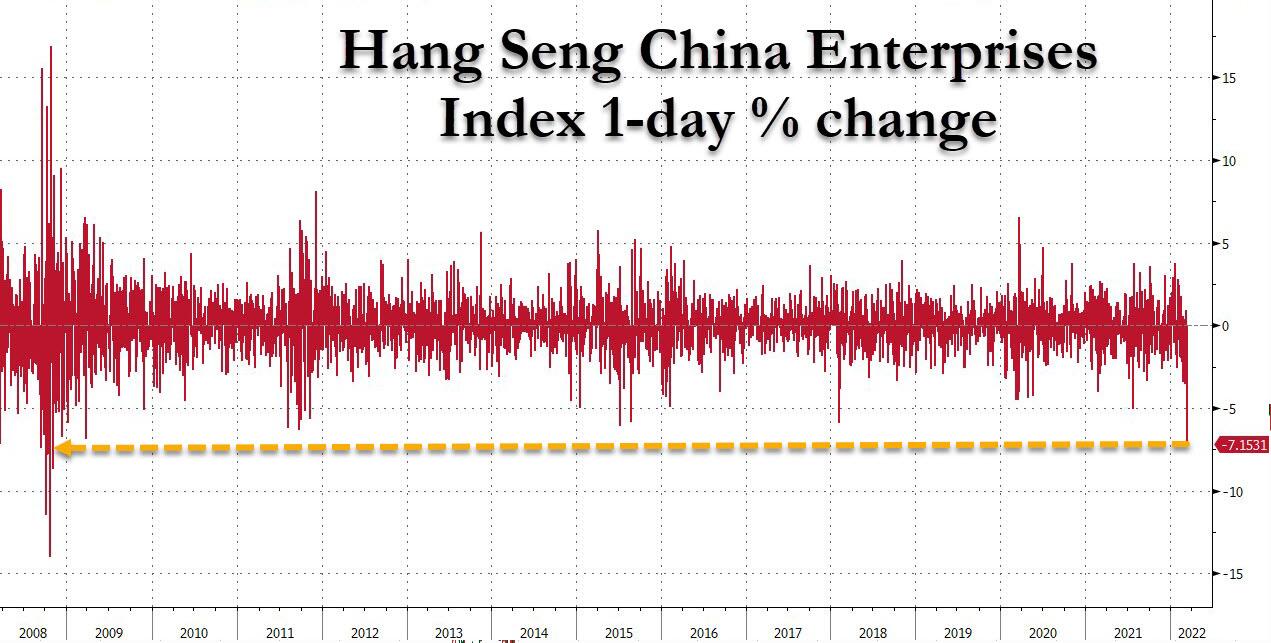

… as the Hang Seng China Enterprises Index closed down 7.2% on Monday, the biggest drop since November 2008.

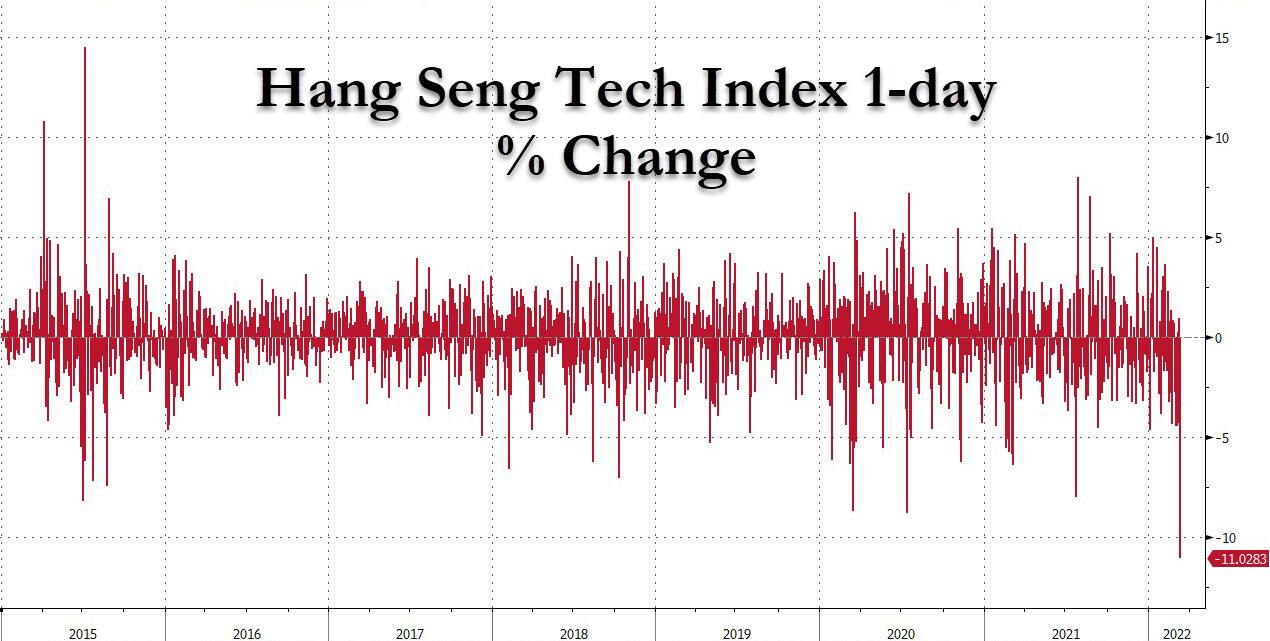

Meanwhile, the Hang Sang Tech Index tumbled 11% in its worst decline since the gauge was launched in July 2020, wiping out $2.1 trillion in value since a year-earlier peak, after the southern city of Shenzhen, a key tech hub near Hong Kong, was placed into lockdown to contain rising Covid-19 infections. The broader Hang Seng Index lost 5%.

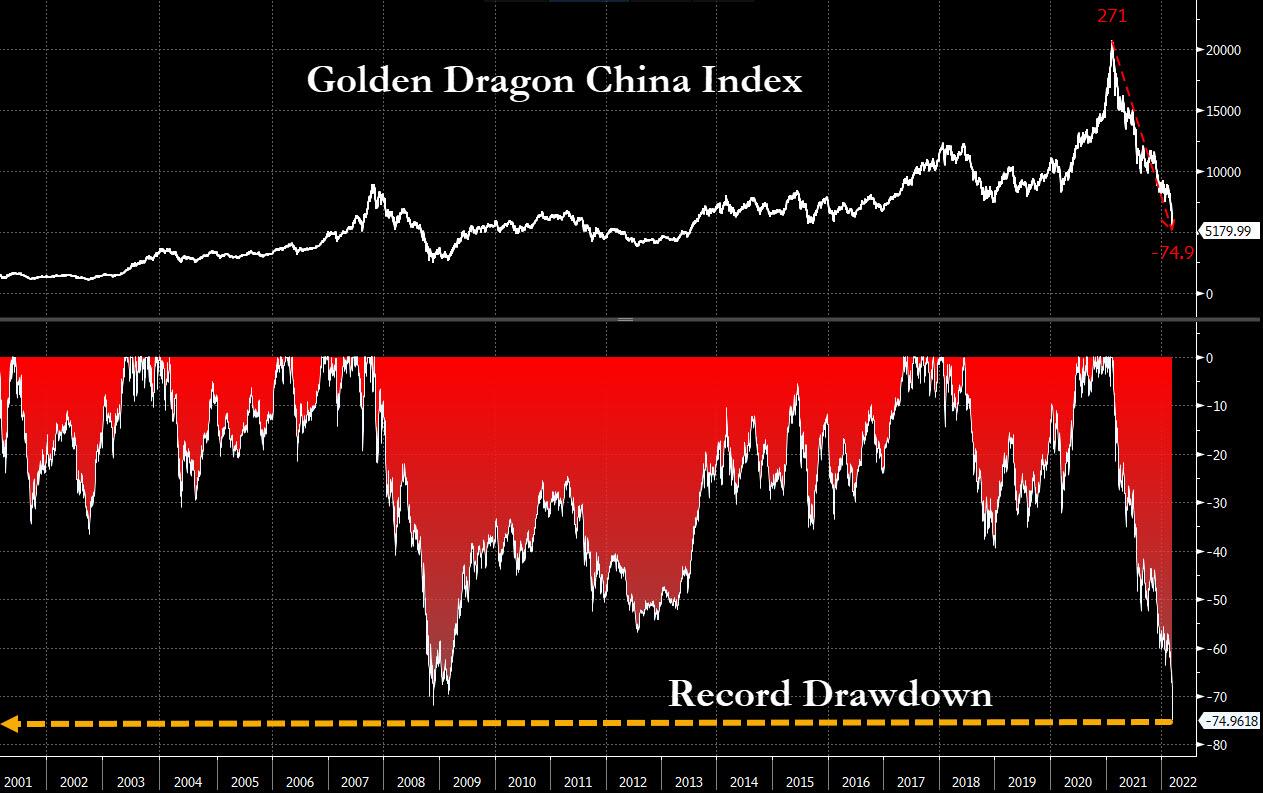

The US-traded Golden Dragon China index tumbled another 12%, taking its drawdown to -75% from its recent all time high, surpassing the drawdown recorded during the global financial crisis!

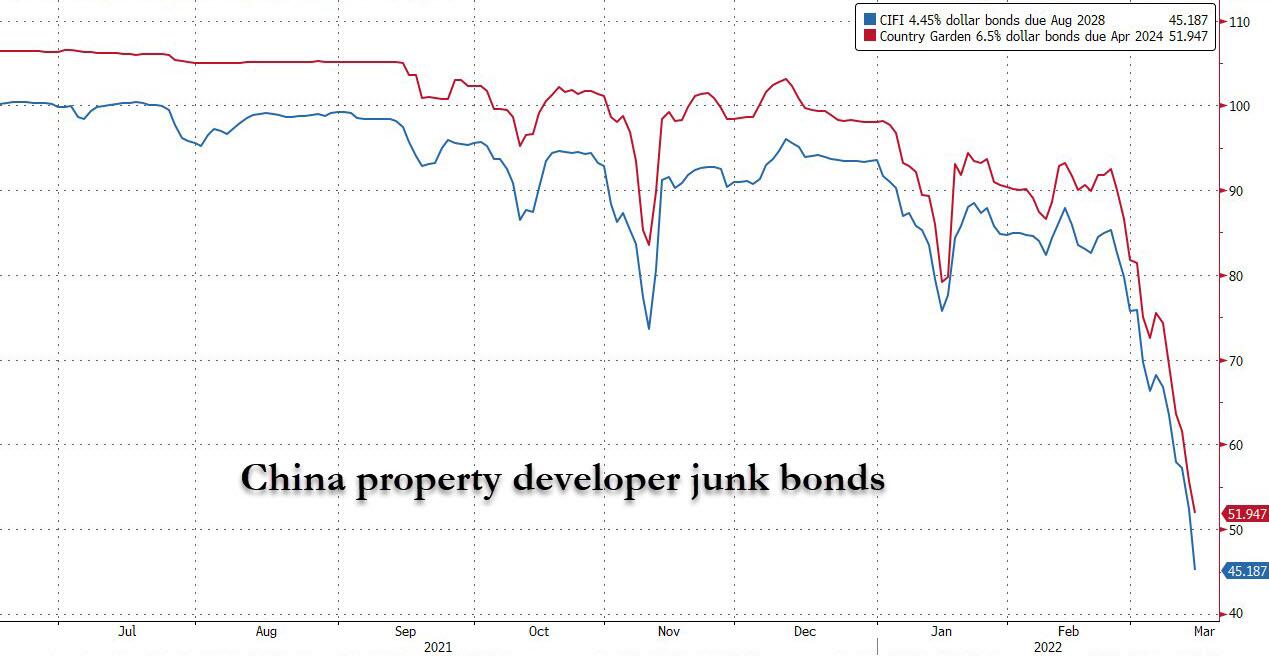

Meanwhile, as discussed last night in “All Hell is Breaking Loose in China“, it wasn’t just Chinese stocks that got taken to the woodshed: Chinese property developer junk bonds were true to their name, and issues by such formerly “solid” companies as CIFI and Country Garden cratered to lowest levels in history, both trading about 50 cents on the dollar as China’s housing sector – which warehouses the vast majority of China’s middle class wealth – is imploding.

Against this cataclysmic background, US futures were initially surprisingly stable, in a rerun of Friday’s hopium trade where traders were expecting some good news out of today’s Ukraine ceasefire negotiations, which however never came. Algos were perhaps also looking at the slide in oil – which had traded recently as a “peace” proxy – and expecting some resolution that would finally short-circuit the surge in commodity costs. And indeed, oil has tumbled almost $30 from its recent highs over $130 to just over $100 today…

… but as the day drew on, it became clear that just like last Friday, there would be no deal, and since the drop in oil was almost entirely due to rising recession fears, stocks resumed their relentless slide.

Meanwhile, a bizarre announcement from Barclays early in the day that the bank would suspend sales and issuance of the VXX ETN led to a furious short squeeze as the key volatility ETN decoupled from its underlying Emini future, and soared higher in the process sparking even more selling from correlation algos, which led to even more upside in the VXX and so on. This particular dislocation will likely persist until Barclays gets a tap on the shoulder as there are countless hedge funds who are short the VXX and will suffer massive losses unless the relationship is normalized.

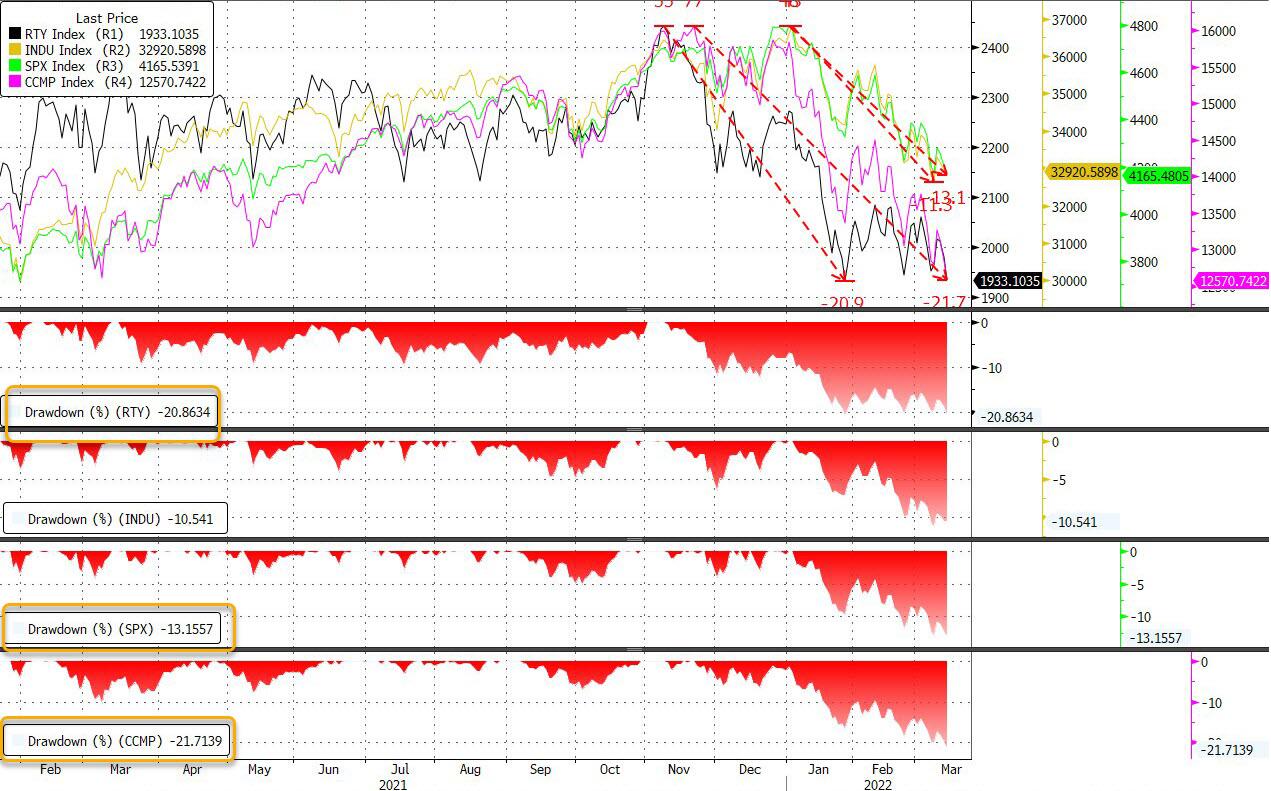

As a result of the broad riskoff shift, drawdowns across all US equity indexes became even more pronounced, dragging the Russell and Nasdaq deeper into bear market territory, and the S&P now down 13% from its all time highs…

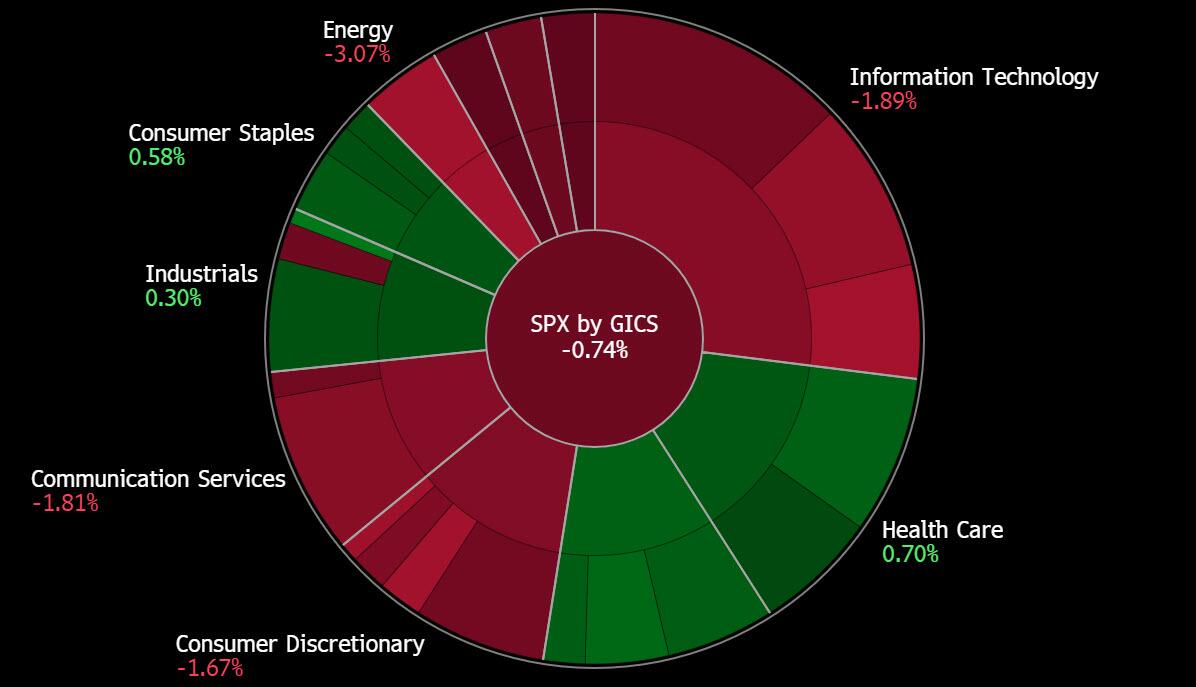

… and while there was carnage everywhere, especially in energy as the YTD best performing sector suffered major losses today, sliding 3% and the day’s worst performer…

… the biggest micro driver was AAPL’s 2.7% plunge, which tumbled to the lowest level since Nov 15 and more importantly, dropped below its key 200DMA critical support for the first time since June 2021 as traders freaked out that the shutdown of the Shenzhen Foxconn factory would lead to a supply chain shock for the world’s biggest company.

Yet despite the widespread carnage, there was none of the traditional flight to safety, because as gold and silver tumbled…

… so did Treasuries with the 10Y yield closing at session highs just shy of 2.15% but more ominously the 5% is right behind and breathing down the benchmark bond’s neck at 2.10%! A few more basis points and the 5s10s will invert confirming what everyone knows: a recession is coming if not already here.

Finally, with the Fed meeting looming in just two days and, instead of pricing in some mercy from Powell, the fed funds market saw even more pain, and now prices in more than 7 rate hikes in 2022 and more than 17% odds of a 50bps rate hike in March in response to what is an inflation tsunami that is only just starting…

… and with it bringing much more pain for stocks in the coming weeks and months.

Tyler Durden

Mon, 03/14/2022 – 16:07

Continue reading at ZeroHedge.com, Click Here.