Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

Treasury Hikes Borrowing Estimate To $1 Trillion This Quarter As It Scrambles To Rebuild Cash

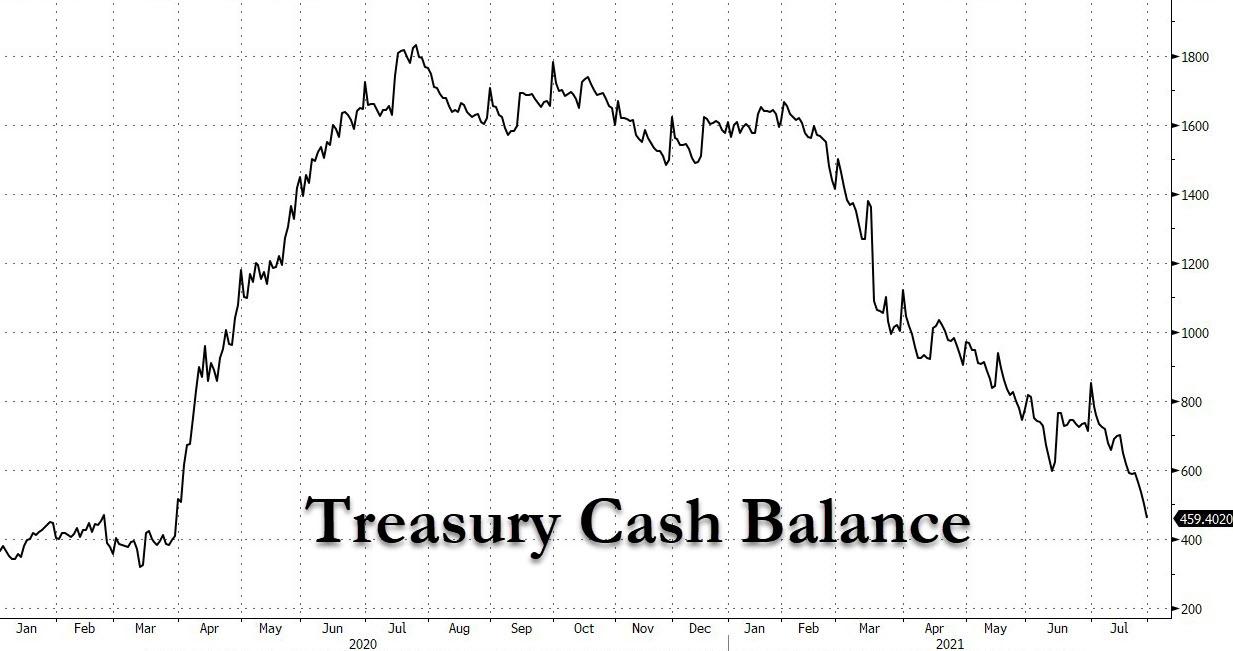

Six months ago, at the start of May when the Treasury was busy spending hundreds of billions of cash parked in the Fed’s Treasury General Account in a form of stealth QE, the US government surprised markets when it announced that it expected to release just $100BN in cash in May and June, bringing its total cash balance to $800BN by the end of June, and then just another $50BN lower three months later, or $750BN at the end of Sept. Additionally, the Treasury assumed a cash balance of approximately $450 billion at the expiration of the debt limit suspension on July 31 based on expected outflows under its cash management policies. And while the Treasury caveat that “the actual cash balance on July 31 may vary from this assumption based on changes to expected outflows in that period” its estimate was surprisingly spot on, with the latest Daily Treasury Statement showing $459 billion as of the end of July, not far from its forecast.

Then, three months later, the Treasury released yet another estimate of Treasury Marketable Borrowing which showed that the Treasury plans on borrowing almost $1.4 trillion in the second half of calendar 2021, it hopes of ending the year with $800 billion in cash – well below the $1.7 trillion in cash it held at the end of 2020 – and last but not least, assumes that a debt limit suspension or increase will be enacted.

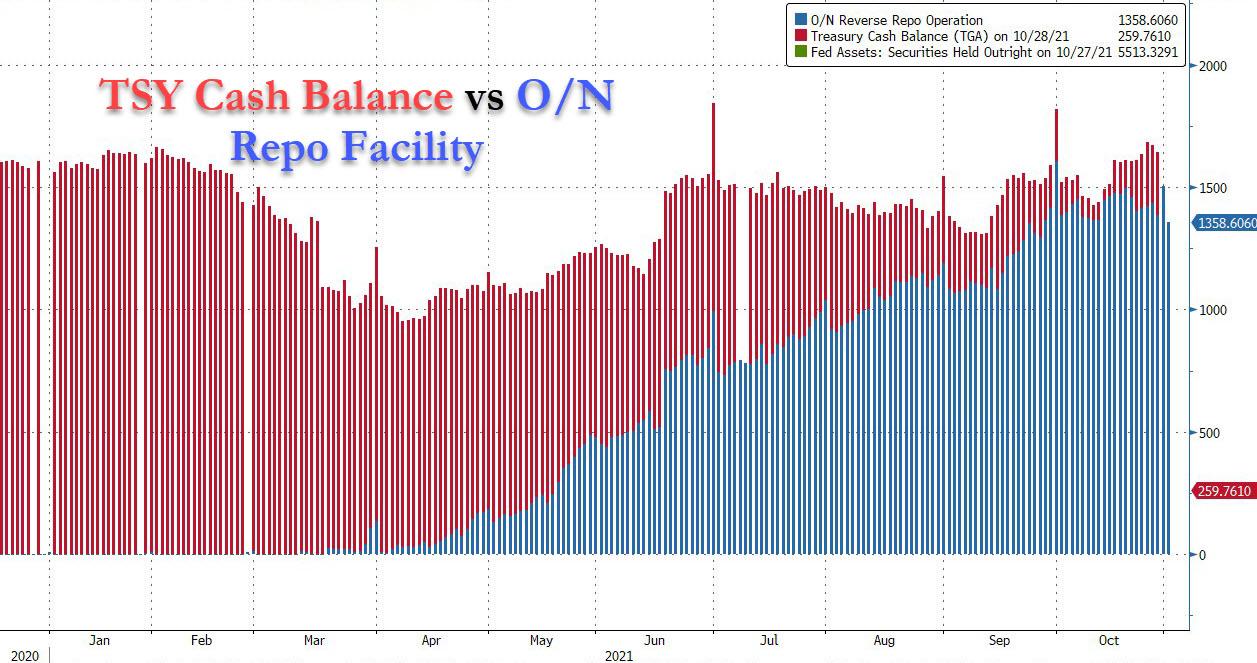

Well, since then the debt ceiling has still not been lifted even if the Biden admin did get a two-month extension until early December, during which it can replenish some of its cash buffer, at which point another vote will be required either kicking the can again on the debt ceiling or lifting it outright. And as a result, the Treasury has been quite busy selling T-Bills and Cash Management Bills and rebuilding in the process draining some of the cash in the repo facility. As a reminder, the total cash holdings between the O/N repo facility and the TGA account have been mostly flate since July, and recent weeks have been no difference; it’s also why overnight the Fed’s reverse repo facility saw the biggest one day drop since Oct 1, as seventy-four participants took down $1.359 trillion, down $143 billion from $1.502 trillion on Oct. 29.

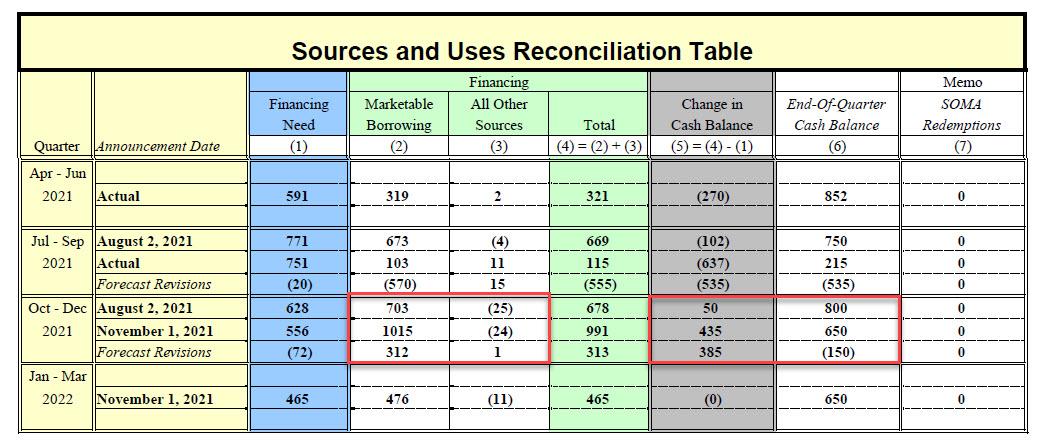

Which brings us to today’s latest quarterly edition of the Treasury’s marketable borrowing estimates, according to which the Treasury plans on issuing $1.015 trillion in net marketable debt in the Oct-Dec quarter, up $312BN from the Aug estimate of $703bln. This increase in borrowing estimates is due to the lower beginning cash balance in the Oct-Dec quarter, which was at just $215BN to start, far below the $750BN forecast in August. And since the Treasury hopes to grow that cash balance by $435BN to $650BN, or much more than the $50BN in cash growth previously forecast, that’s why the Treasury is expecting far greater net issuance this quarter.

In other words, the $385BN in additional cash this quarter will come from an incremental $312BN in additional net issuance. All of this is shown below:

Here is the breakdown directly from the Treasury:

- During the October – December 2021 quarter, Treasury expects to borrow $1,015 billion in privately-held net marketable debt, assuming an end-of-December cash balance of $650 billion. The borrowing estimate is $312 billion higher than announced in August 2021, primarily due to the lower beginning of quarter balance, somewhat offset by a lower end-of-quarter balance and higher receipts.

- During the January – March 2022 quarter, Treasury expects to borrow $476 billion in privately-held net marketable debt, assuming an end-of-March cash balance of $650 billion.

Of course, since far less cash was raised in the past quarter due to the continued debt ceiling overhang, during the July – September 2021 quarter, Treasury borrowed only $103 billion in privately-held net marketable debt (and ended the quarter with a cash balance of $215 billion). This is $570 billion less than the amount the Treasury had originally estimated back in August, when it forecast $673 billion in net marketable borrowing and assumed an end-of-September cash balance of $750 billion. The $570 billion decrease in borrowing resulted primarily from the decrease in the end-of-September cash balance and, to a less extent, from an increase in receipts and a decrease in expenditures.

The original and revised Treasury cash forecast is below – it shows that the Treasury now expects total cash to rise from $260 billion currently to $650 billion by year end.

The practical implications are familiar and similar to what we discussed last quarter: this continued cash rebuild is the equivalent of a liquidity drain, however since we are now seeing a liquidity shift out of the Repo facility and into the TGA, it likely won’t have much of an impact on asset prices at least until such time as the Fed’s taper and/or rate hikes also become a factor..

Tyler Durden

Mon, 11/01/2021 – 15:39

Continue reading at ZeroHedge.com, Click Here.