Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

Where Will The Next Deflationary Shock Come From?

Authored by Louis-Vincent Gave via Evergreen Gavekal blog,

“Whenever I hear numbers like this, I look back to my childhood growing up in Hungary, where…[the] value of money meant nothing. I’m very worried this is an unstoppable situation because the longer the Fed waits, the more they will have to raise rates. So, we’re basically painting ourselves into a box, and I don’t see how we’re going to get out of it.”

– Thomas Peterffy, chairman and founder of Interactive

The 1986 oil price crash, to an extent, fired the starting gun on 30 years of global deflation. As commodity prices collapsed, so did the Soviet Union, giving the West a deflationary peace dividend. By the early 1990s, Japan’s real estate and equity market busts threatened its banks. The rollout of the North American Free Trade Area and the 1995 “tequila crisis” helped make Mexico a competitive manufacturing hub. Soon after, the 1997-98 Asian crisis made producing abroad even cheaper, while China’s 2001 entry into the World Trade Organization greatly simplified outsourcing. In 2008, the US mortgage bust spurred China to build more infrastructure, unleashing 500mn more workers into the global economy. Europe’s 2011-13 crisis caused another deflationary hit, while the US’s shale energy boom stopped oil and gas prices rising.

So today, as inflation expectations move toward generational highs, a relevant question is: where might the next deflationary shock come from?

Europe.

If vaccine rollouts let Europeans vacation freely this summer, it is unlikely to spur deflationary forces. The effect should be steeper eurozone yield curves, outperformance by financials and a firmer euro. Yet, if Europeans are told to stay home, another deflationary eurozone crisis could still ensue. Citizens deprived of a vacation may register their protest at the ballot box or, more likely, on the streets. For this reason, the odds are high that Europe re-opens, just as last year’s large fiscal stimulus gets rolled out. We should thus assume that—for now at least—Europe will not be a deflationary black hole.

Commodities.

With Europeans set to hit the beach and Americans looking to crank up the vehicle miles, energy prices should stay well bid. And as about a third of the cost of producing commodities is attributable to energy, the broader complex is unlikely to provide any kind of deflationary shock in the near future.

The US dollar.

As big projects in emerging economies are mostly funded in US dollars, any strengthening of the unit reduces their growth and depresses commodity prices. So, could a rising dollar unleash deflationary forces? For now, the US currency is making lower highs and lower lows, in spite of higher yields. This is perhaps not surprising, as the Federal Reserve has promised to add US$120bn of fresh dollars to the global system each month. Given such generosity, the threat of a US dollar short squeeze has now greatly receded. Hence, the dollar seems unlikely to be a deflationary force in the near future.

The renminbi.

With so much production capacity centered in China, the renminbi’s value is vital for manufacturers. When it is weak, few Western industrial firms can compete with China but when strong, foreign producers can expand margins and/or compete on price. Whether viewed on a three-year, five-year or 10-year basis, the renminbi has been the world’s best-performing major currency on a total return basis, which shows that, structurally, there is little appetite in Beijing for a devaluation. Moreover, as China’s trade surplus hits new highs and the authorities there tighten both fiscal and monetary policies, there seems little reason, cyclically, for this to happen.

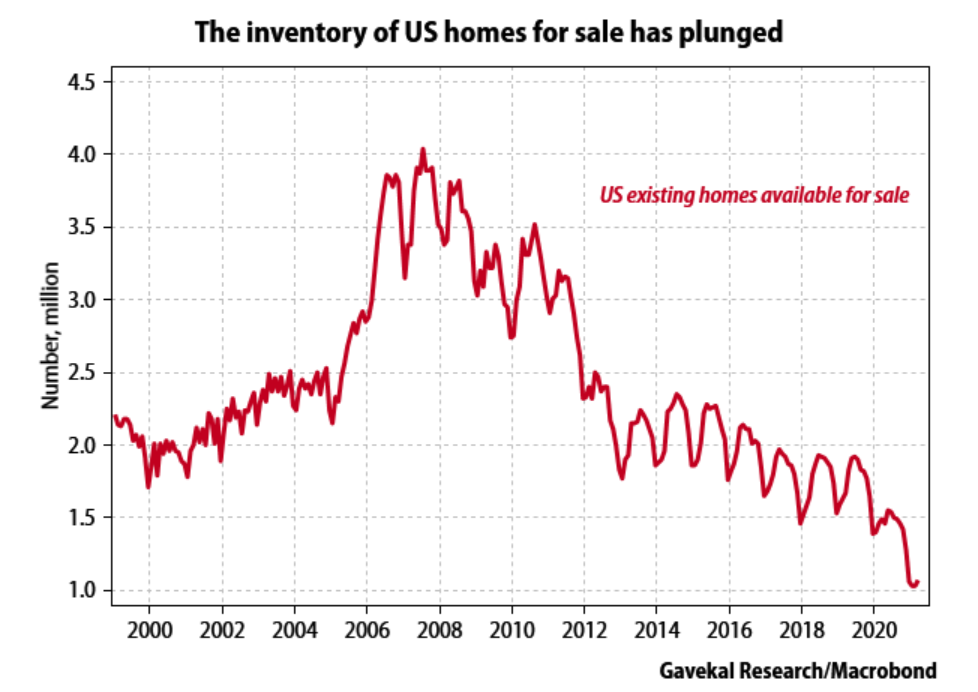

US real estate.

Homes are getting expensive, with median prices relative to incomes near the highs seen in 2006-07. The difference now is low supply as the stock of existing homes available for sale is at an all time low. Add into the mix the soaring cost of skilled labor and surging prices for building materials and it is hard to see why US real estate prices should crater anytime soon.

Putting it all together, in the coming few years those “usual suspects” that previously unleashed deflation are now more likely to raise the inflationary temperature. Hence, if deflationary forces are going to carry the day, there will need to be impressive productivity gains. Somewhere in the system, someone will have to produce a whole lot more, with a whole lot less. But is this likely given the following trends that have been covered in recent Gavekal reports?

-

Globalization rollback: productivity gains from outsourced production are under threat as its true social costs have become more apparent.

-

Semiconductor shortage: robots have been touted as replacements for low-end labor everywhere, but as car factories are shuttered for want of chips one has to wonder where robot-makers will find the semiconductors they need to build the robots that will then build the cars.

-

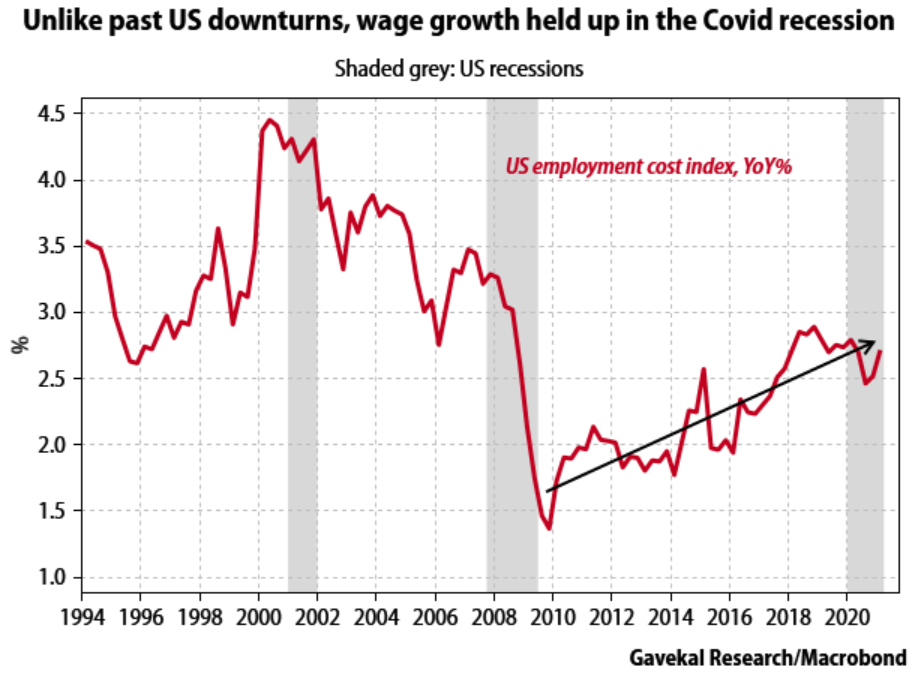

Labor markets: workers across Western economies are being incentivized to stay home and, unsurprisingly, wages are now starting to rise. Indeed, 2020 saw the first meaningful US recession in which wage growth barely fell.

This leaves us in the situation of seeing the price of everything from meat, corn, gasoline and lumber to shipping rates rise without a clear countervailing deflationary force. In an environment of rising government intervention, expanded public hand-outs, higher corporate taxes and more protectionism (and that is just the US!), it is possible that a surge in productivity provides an offset to the growing inflationary wind. But like an Elizabeth Taylor marriage, this seems to represent the triumph of hope over experience.

Tyler Durden

Sat, 05/29/2021 – 16:30

Continue reading at ZeroHedge.com, Click Here.