Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

The Energy Rally Is Likely Premature

Tyler Durden

Fri, 12/04/2020 – 15:26

Authored by Lance Roberts via RealInvestmentAdvice.com,

The rally in energy companies is likely premature. To understand why such may be the case, we have to review a bit of history.

In 2013, I began warning about the risk to oil prices due to the ongoing imbalances between global supply and demand. Those warnings fell on deaf ears as no one paid attention to the fundamentals. Then, with near-zero interest rates, banks, hedge funds, and private equity firms were chasing “yield” in the energy space. Naturally, with money flooding into the system, companies drilled economically unproductive wells to meet investor demands, which drove supplies higher.

A Bit Of History

It didn’t take long for previous predictions to play out. In May of 2014, I wrote:

“It is quite clear the speculative rise in oil prices due to the ‘fracking miracle’ has come to its inglorious, but expected conclusion. It is quite apparent some lessons are simply never learned. “

Since then, OPEC has engaged in repeated rounds of cutting production to support oil prices. While there was a short-term success from those actions, ultimately, U.S. “shale” producers outpaced those cuts with new supply. In September of 2017, we again reviewed the fundamentals warning investors of the risk.

“While there is hope production cuts will continue into 2018, a bulk of the current price gain has likely already been priced in. With oil prices once again overbought, the risk of disappointment is substantial.”

Then, as 2018 came to a close, I made an important observation:

“Prices of both energy-related shares and oil have been disappointing. The expected decline in oil prices is more important than just the relative decline in share prices of energy-related stocks. Energy prices are highly correlated with economic activity.“

That bit of history helps frame our reasoning why the rally in energy stocks is likely premature. The fundamental issues of supply, demand, sector debt, and weaker economic growth rates remain problematic.

Economic Recovery Will Remain Weak

The 33% surge in economic growth in Q3 was certainly welcome. However, the recovery was not a function of organic activity. Instead, it was a function of massive Government stimulus which pulled forward future consumption.

As is always the case with Government largesse, recycling “tax dollars” may appear to create activity. However, the illusion quickly fades along with the stimulus. Such is why, despite zero interest rates and Central Bank interventions, economic growth rates continue to decline. As we showed previously:

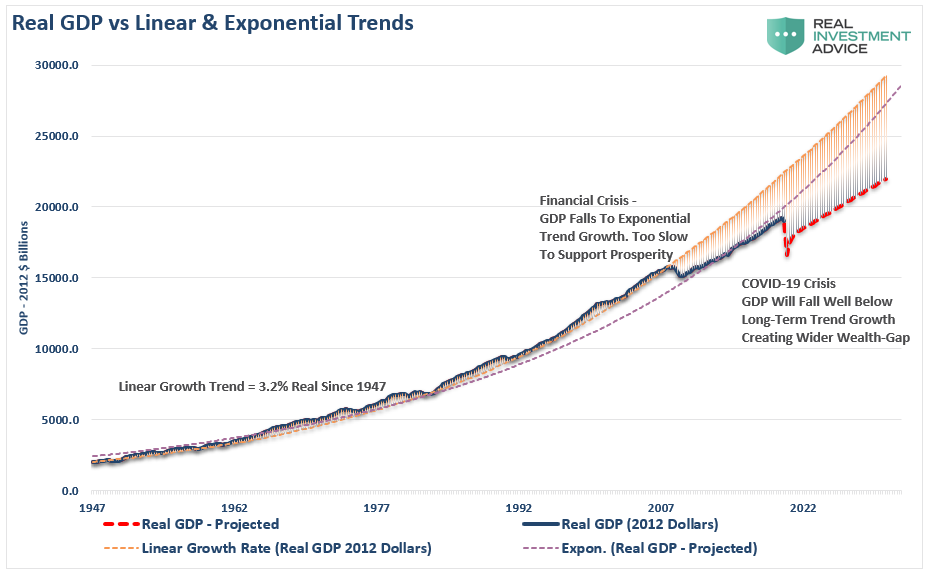

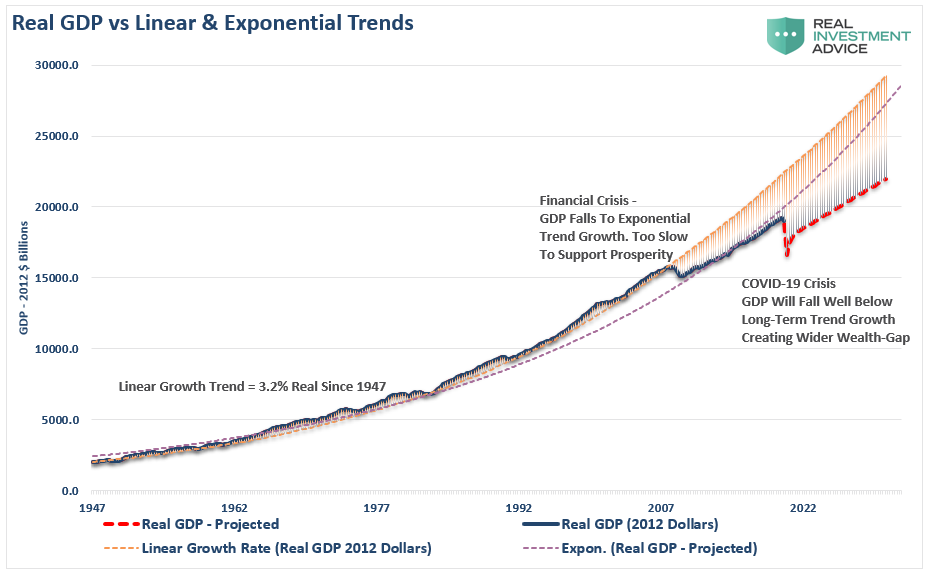

“Before the ‘Financial Crisis,’ the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.”

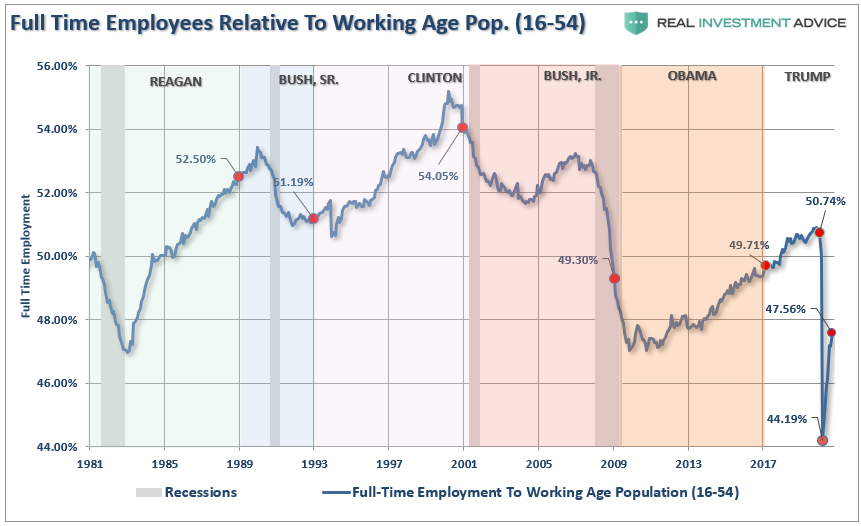

Unfortunately, when the current recession ends, economic growth rates will again run at a slower trajectory. Such will translate into weaker wage growth and suppressed full-time employment-to-population ratios.

“Companies’ fast adoption of technology, along with increased productivity and change in demand, will further retard employment in the ‘New-New Normal.’

To generate economic growth and prosperity, ‘full-time’ employment is critical. After the ‘Financial Crisis,’ the number of ‘full-time’ jobs relative to the population collapsed and only recovered about half of what was lost. We witnessed the same following the ‘dot.com’ crash. It is highly likely that ‘full-time’ employment will take another stop down as weaker demand requires fewer full-time staff.”

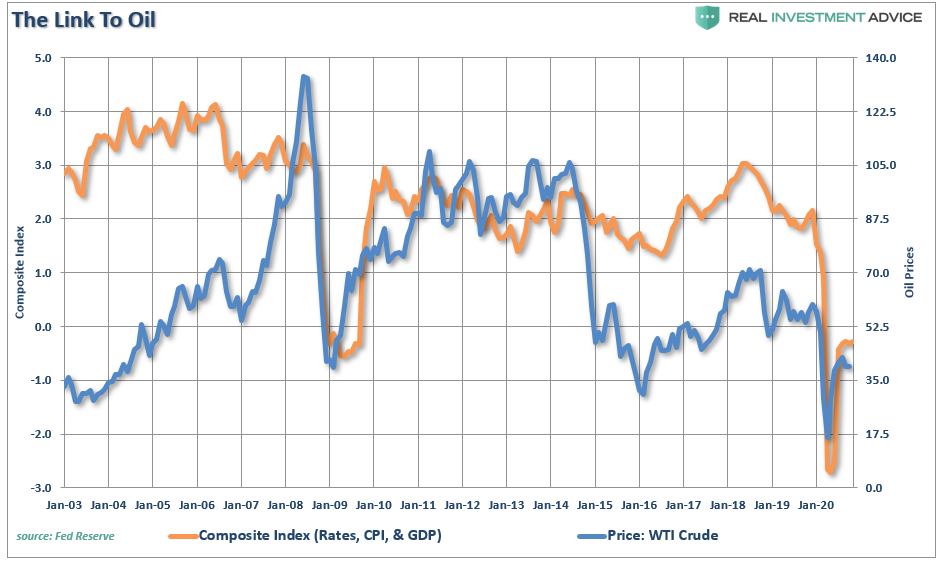

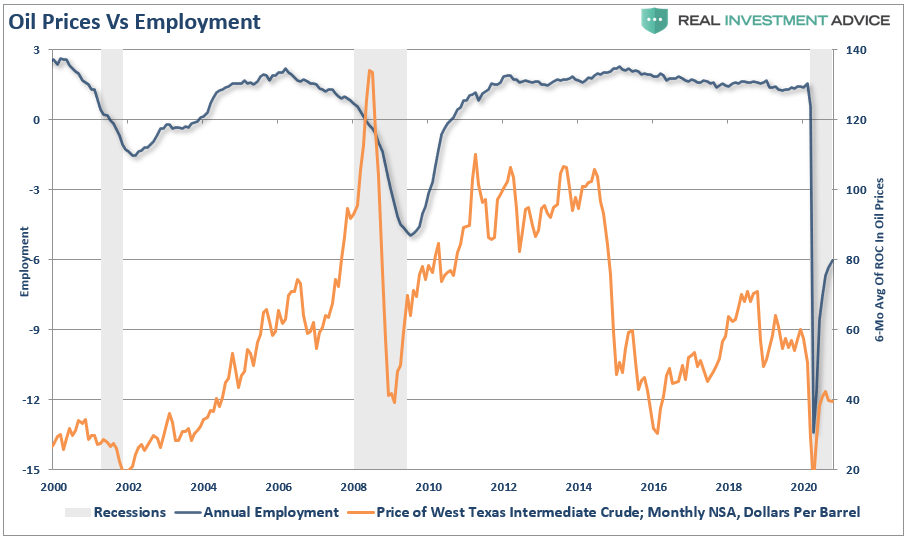

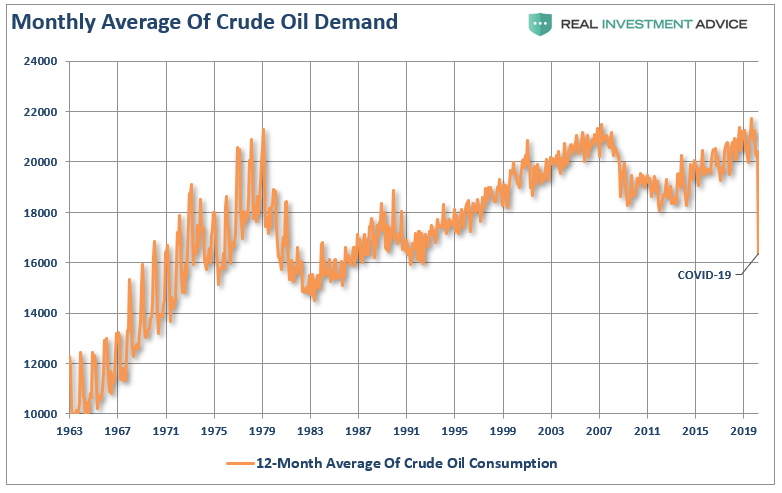

Oil Tied To The Economy

Oil is a highly sensitive indicator relative to the expansion or contraction of the economy. Virtually every aspect of our lives impacts oil consumption. The equation’s demand side is a tell-tale sign of economic strength or weakness, from the food we eat to the products and services we buy.

The chart below combines interest rates, inflation, and GDP into one composite indicator to provide a more obvious comparison to oil prices.

It should not be surprising that sharp declines in oil prices have been coincident with downturns in economic activity, a drop in inflation, and a subsequent decrease in interest rates.

There is also a not so insignificant correlation between oil prices and employment. The energy sector produces many, and some of the highest wage paying, jobs in the country.

When it comes to employment, most of the jobs “created” since the financial crisis has been lower wage-paying jobs in retail, healthcare, and other service sectors of the economy. Conversely, the jobs created within the energy space are some of the highest wage paying opportunities available in engineering, technology, accounting, legal, etc.

Each job created in energy-related areas has had a “ripple effect” of creating 2.8 jobs elsewhere in the economy from piping to coatings, trucking and transportation, restaurants, and retail.

Drilling for oil also requires sizable capital expenditures, which has a large multiplier effect on the economy. (Politicians need to be careful not to “kill the golden goose.”)

With economic weakness gaining traction globally, it is hard to justify an improving outlook for oil given the backdrop of “Too much supply. Too little demand.”

Unfortunately, supply is set to rise.

Drill Or Die

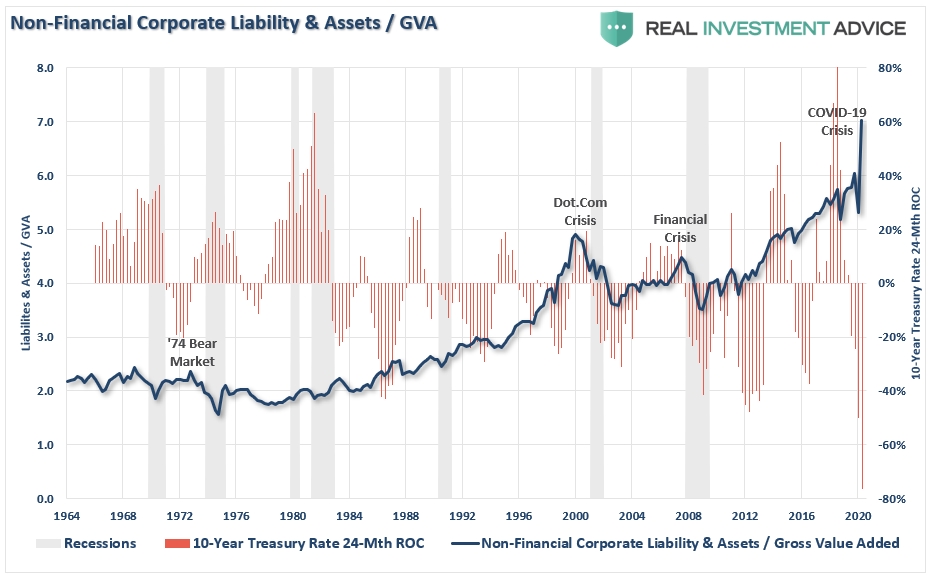

I recently wrote about corporate debt and the rise of “zombie companies” caused by a decade of Federal Reserve interventions and bailouts.

“Given the Federal Reserve’s monetary injections and suppression of interest rates, it is not surprising to see companies leveraging their balance sheets. As interest rates have plunged, corporations have hit a record issuance of debt to pay dividends and other non-productive purposes.” – The Lack Of Value In Value

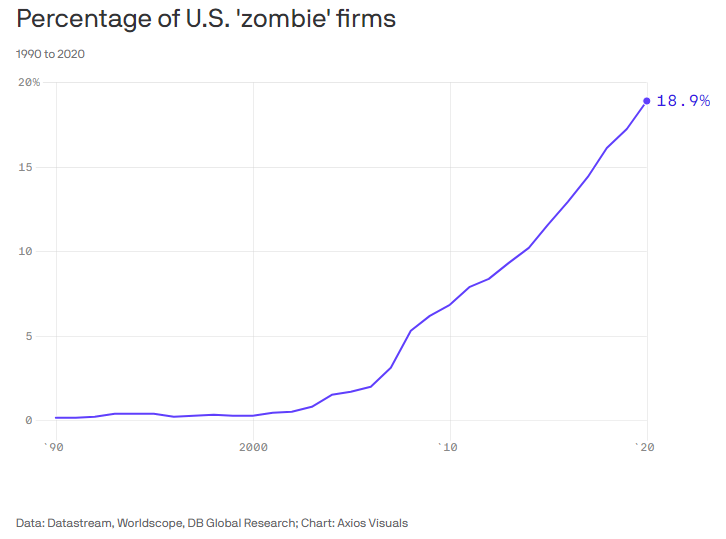

The surge in debt, which is supported by the Federal Reserve’s ongoing generosity, has led to a large number of “zombies.”

‘Zombies’ are firms whose debt servicing costs are higher than their profits but are kept alive by relentless borrowing.

Such is a macroeconomic problem. Zombie firms are less productive, and their existence lowers investment in, and employment at, more productive firms. In short, a side effect of central banks keeping rates low for a long time is it keeps unproductive firms alive. Ultimately, that lowers the long-run growth rate of the economy.” – Axios

Many of these “zombies” exist in the energy space.

These companies that took on the debt, or equity, to drill must keep drilling to generate revenue or die. As supply increases, prices decline, leading to further drilling losses in wells, which were only marginally profitable, to begin with. Companies then have to take on more debt to remain operational, further increasing supply in hopes that prices will eventually rise.

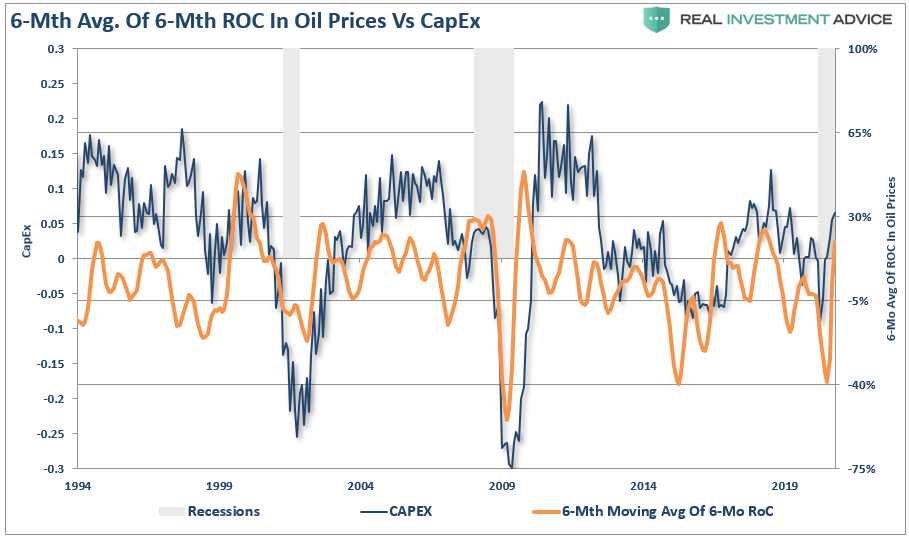

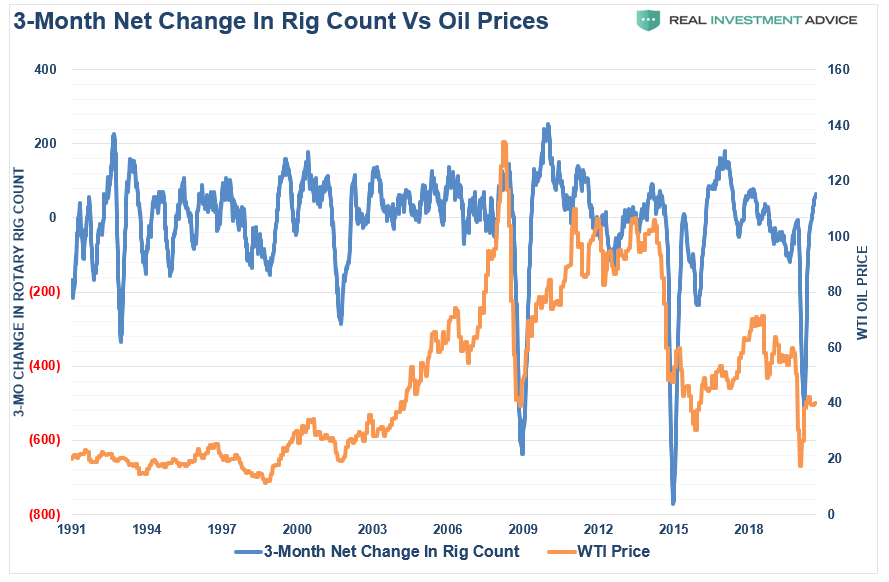

The chart below shows that even minor upticks in oil prices lead to rigs’ rapid deployment to produce more oil, increasing the supply.

While logic would suggest companies actively reduce the supply to increase prices, operators cannot “shut-in” production due to the loss of needed operating revenues. The underlying land leases also constrain them.

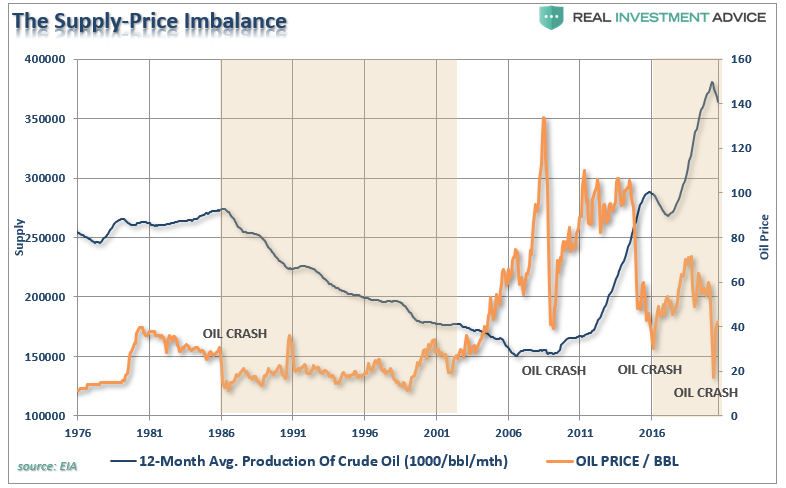

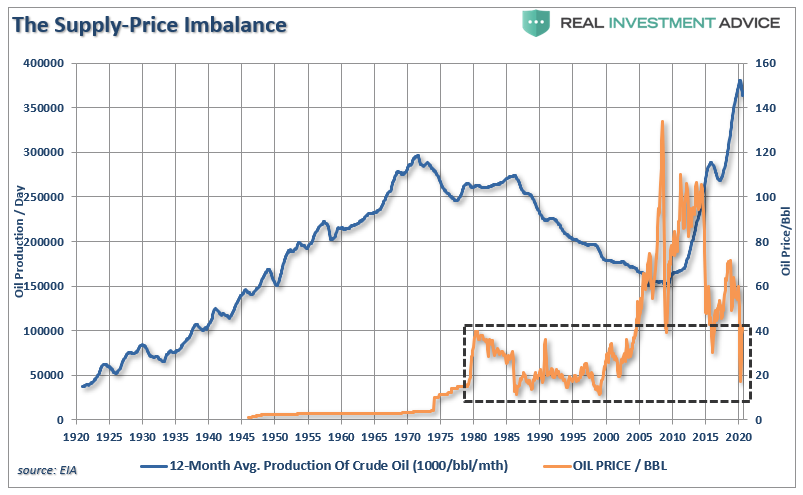

The Supply-Demand Imbalance

The current levels of supply create longer-term issues for prices globally. Compounding the problem is weaker global demand due not to just the “economic shutdown” but ongoing issues related to demographics, energy efficiencies, and debt.

The issue remains supply. Despite the crash in oil prices this year, and continued production cuts by OPEC, and nearly 100 energy companies filing bankruptcy, supplies only marginally declined.

Oil production remains near the highest levels in history.

As noted above, oil companies must produce oil to generate revenues with which to operate. For many smaller energy companies, shutting down production is not an option as it would immediately lead to credit defaults and bankruptcies.

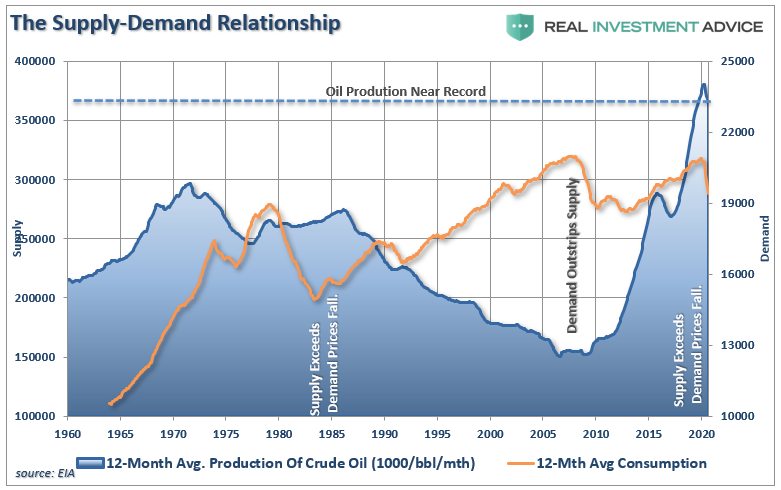

In 2008, when prices crashed, the supply of into the marketplace had hit an all-time low while global demand was at an all-time high. Remember, the fears of “peak oil” was rampant, and oil prices soared higher on concerns about a shortage. However, following the “Financial Crisis,” the “fracking miracle” was launched. Supply surged, usurping the demands of a weaker “post-crisis” global economy.

The supply-demand problem remains even despite the “pandemic” related drop in demand. However, OPEC+ is looking to increase output, which will further exacerbate the supply overhang.

“OPEC + has decided to add another 500 thousand bpd to the current production cut of 7.7 million bpd in Jan. It has agreed that OPEC + will hold another meeting, but not to increase more than 500 thousand bpd.” – Reza Zandi

The Demand Disruption

Then there is the demand side of the equation.

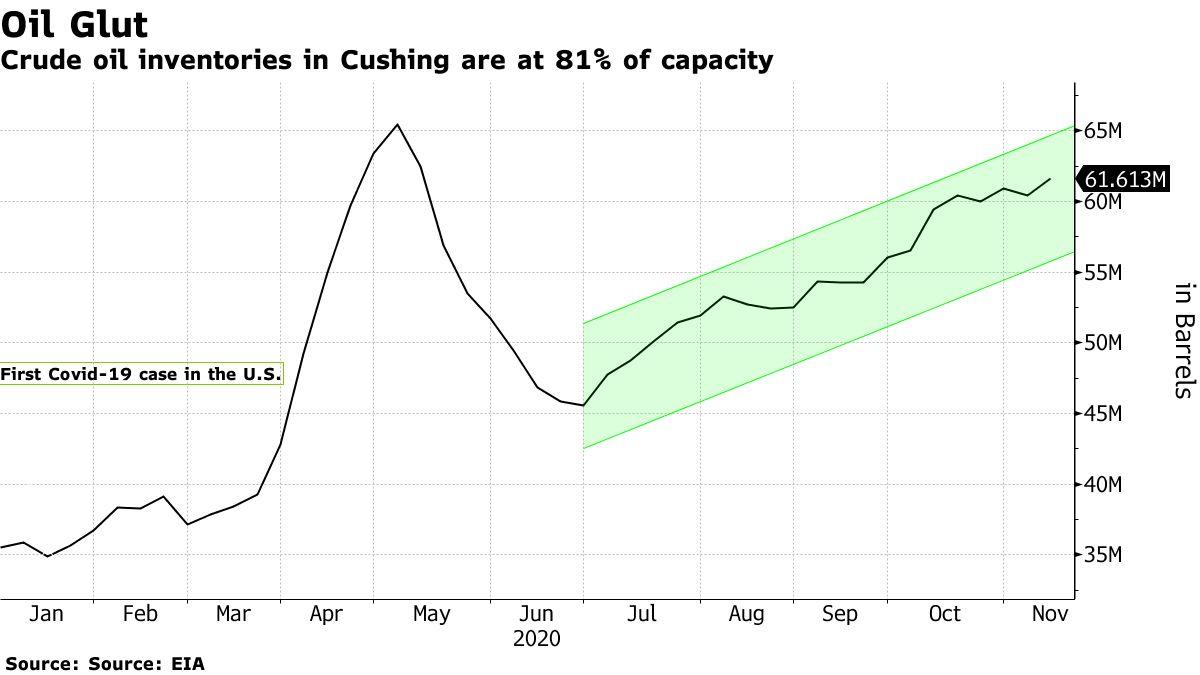

Of course, the problem with dropping demand is that it exacerbates the “supply glut,” leading to continued oil price suppression. Now, it is also leading to a “storage problem” with supplies overwhelming the storage available.

As noted by Bloomberg recently:

“Oil tanks in America’s most important crude storage hub are filling to the brim once again, quickly approaching the critical levels reached in May after prices crashed.

Stockpiles at Cushing, Oklahoma, the delivery point for West Texas Intermediate futures, stood at 61.6 million barrels as of Nov. 13, or about 81% of capacity, according to the most recent U.S. government data. That’s 3.83 million barrels shy of the levels seen in May.”

There are several reasons why demand likely won’t recover back to levels that would absorb the current over-supply issue.

-

Weak economic global growth will continue due to continued increases in debt.

-

The slow and steady growth of renewable/alternative sources of energy

-

Improving efficiencies in energy consumption (EV’s, hybrids, solar, wind, etc.)

-

Technological improvements in energy production, storage and transfer, and;

-

A rapidly aging global demographic

All this boils down to a longer-term, secular, and structurally bearish story.

Conclusion

While many hope for a “V-shaped” recovery, this will likely not be the case after reopening the economy. The “virus” was only the anticipated catalyst that triggered the economic recession.

For all of these reasons, the recent “exuberance” in chasing energy companies is likely misplaced. In reality, there is likely a lot less “value” in the sector than many currently believe.

However, unless there is a reduction in supply and thorough cleansing of the energy sector, the longer-term issues will continue to weigh on energy companies into the future. Ultimately, producers will opt into making cuts, or market dynamics will make the cuts for them. Making a choice is always much less painful than having no choice at all.

You probably don’t want to be overexposed to the sector when that happens.

Continue reading at ZeroHedge.com, Click Here.