Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

Market Turmoil Leads To First Pulled Junk Bond Deal Since July

Tyler Durden

Wed, 09/23/2020 – 17:20

Two weeks ago, when we noticed that for the entire month of August the Fed had not bought a single bond ETF, we asked if Powell was sending the markets a message. Now, with the S&P500 on the verge of a correction, the Nasdaq down 12% from its recent all time high, and traders realizing that the shift in risk sentiment is getting worse by the Fed, the answer appears to be yes.

And while stocks today suffered their worst drop since June, the turmoil in equities is starting to spread culminating in Aethon United BR, a Texas-based natural gas company, postponing a $700 million high-yield bond sale that would have refinanced existing debt. The deal – which comes at a time when junk-rated companies have been binging on debt like never before thanks to the Fed’s pledge to backstop corporate bond markets – was the first to be yanked from the U.S. high-yield bond market since July, when Diamond Resorts pulled a $525 million offering, according to data compiled by Bloomberg.

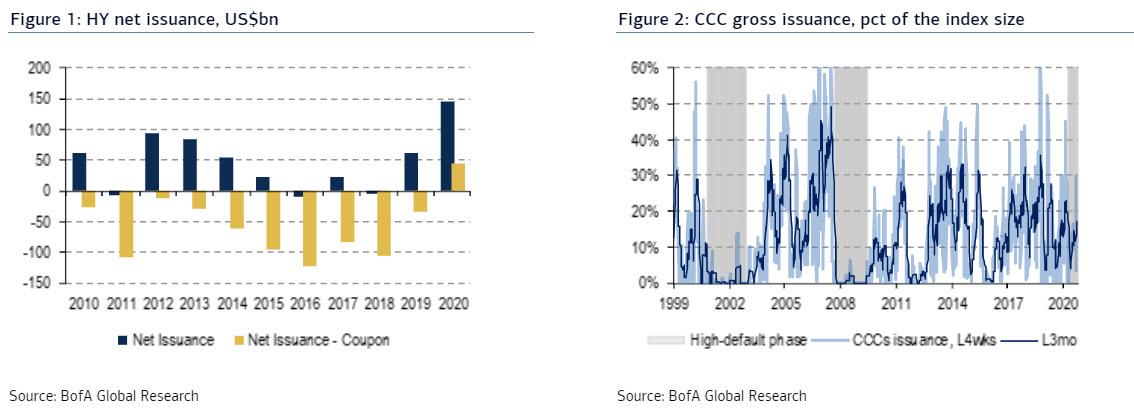

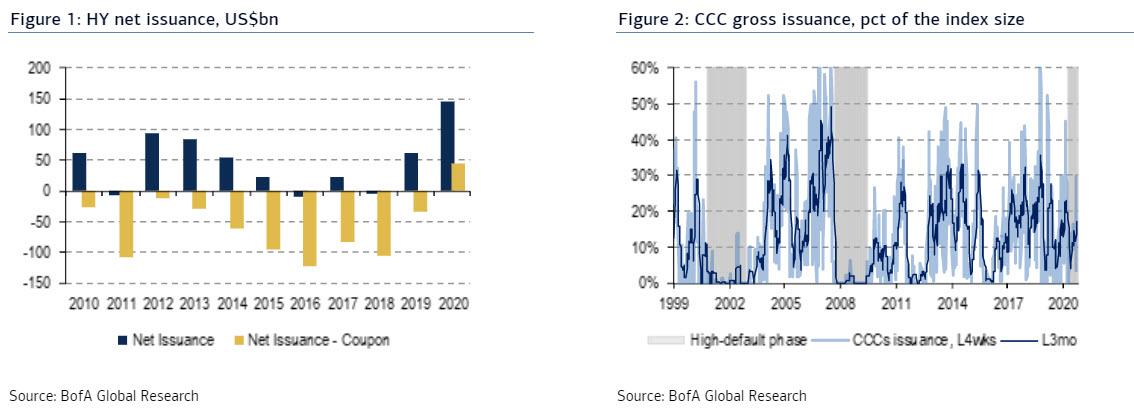

Yet while buying sentiment across the corporate bond market has certainly eased back in recent days, issuance of junk-rated securities is on track to break an all-time record on Wednesday. According to Bank of America, through last Friday, HY gross issuance was $321 billion and about to break its all-time full-year issuance record of $322 billion set in 2012 (BofA’s forecast remains at $375bn for the FY 2020, which would leave us at 1.2x of previous record, with a risk of further upside).

The picture is even more dramatic in net issuance terms, which we define as the difference between gross issuance and calls/tenders/maturities. So far in 2020, the net issuance has reached $119bn, already breaching the previous all-time full-year record of $94bn set in the same year 2012. For the FY 2020 we are projecting net issuance at $145bn, which would represent 1.5x of the previous record, if materialized.

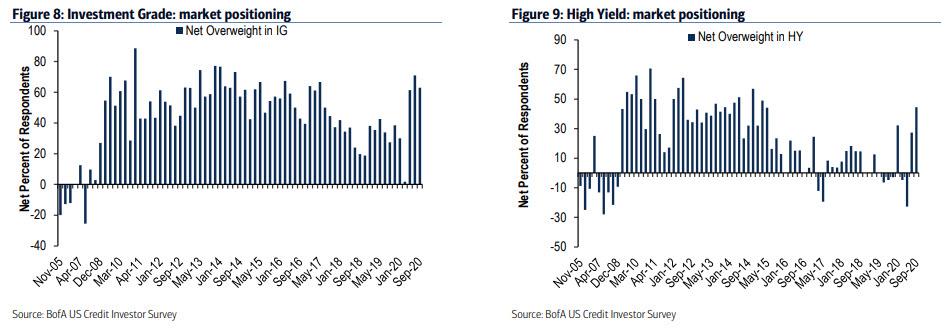

A recent credit market survey from Bank of America found that net overweight positioning in Investment Grade remains elevated at 63% in the September survey, while high yield net positioning increased to a net 44% overweight in September from a net 27% underweight in July and the highest since

This investor euphoria is why even some of the companies most severely impacted by business disruptions caused by Covid-19 have been able to tap debt markets to refinance maturing obligations or add cash to their balance sheets.

However, that tide is now reversing at a dramatic pace, and Aethon may be the canary in the coalmine as the junk bond issuance window slams shut. The company had been sounding out potential investors for the five-year bond sale at a yield in the high 8% to 9% range and originally expected to price the transaction on Sept. 17, according Bloomberg. It had planned to use proceeds to repay an existing second-lien loan and borrowing under its revolver.

The rating agencies had rated the proposed bond single-B, smack in the middle level of junk. Aethon is expected to burn cash through 2021 as it invests in growing production, according to Fitch Ratings.

The question now is how long with the junk bond primary market window remains shut, and who and when will take us over the record junk bond issuance hump of $322 billion.

Continue reading at ZeroHedge.com, Click Here.