Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

Netflix Slides After Subscriber Guidance Misses Estimates

Recent earnings reports from streaming giant Netflix have been a mixed bag: the stock tumbled three quarters ago when the company reported earnings for its first full “post Corona” quarter and warned that “growth is slowing”, before again plunging three quarters ago when the company reported a huge miss in both EPS and new subs, which at 2.2 million was tied for the worst quarter in the past five years, while also reporting a worse than expected outlook for the current quarter. This reversed two quarters ago when Netflix reported a blowout subscriber beat and projected it would soon be cash flow positive, sending its stock soaring to an all time high – if only briefly before again reversing and then tumbling last quarter when Netflix again disappointed when it reported a huge subscriber miss and giving dismal guidance.

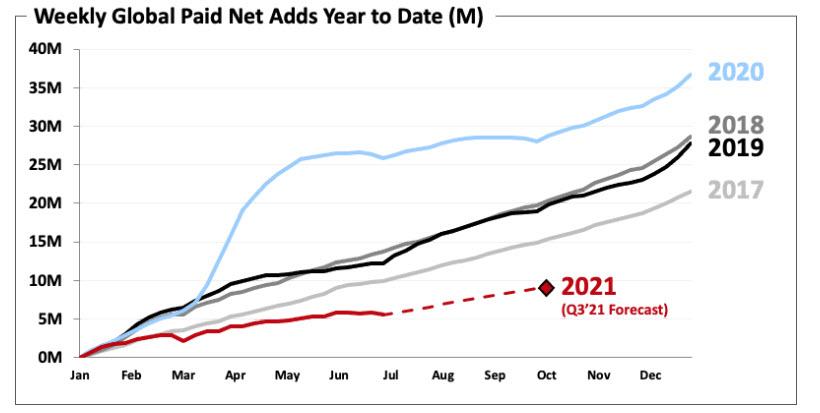

Which brings us to today, when investors are on edge today to find out not whether the company would beat or miss expectations, but rather if the slowdown CEO Reed Hastings warned about is for real and has pulled forward even more subscribers due to covid? After all, Netflix has been warning for months that growth would slow in 2021 compared to the phenomenal signup rate at the start of the pandemic lockdown last year. And yes, brace for a huge base effect hit: in the second quarter of 2020, the service added 10 million new customers, second only to the 15.77 million it added in the record first quarter of 2020.

To be sure, despite a series of hit or miss earnings, the company has been riding a wave of optimism, its stock soaring in early 2021. Still, after hitting to a record high in January, the stock has traded rangbeound, unable to break out to a new high, for the past seven months. And while there’s no doubt that viewership has surged during the Covid-19 lockdowns in the U.S. and much of the world, there are complications: the virus has brought TV and film production to a halt, a situation that may only get more dire for Netflix as the months wear on. But the biggest question remains how many future subs has covid brought to the present, and tied to that – will the panic over the Delta strain lead to another mini burst in subscribers in the coming quater(s)?

Indicatively, consensus expects just 1.12 million new subscribers to be added in the second quarter, just above the company’s own projection of 1 million new subs. Revenue are expected to come in at $7.32 billion, up from $7.16 billion last quarter, and resulting in EPS of $3.36, down slightly from last quarter’s $3.75. This, as streaming video remains on a hot streak since the pandemic struck.

Previewing the quarterly result, Bloomberg Intelligence analysts Geetha Ranganathan and Amine Bensaid cautioned that Netflix’s massive 2020 is leading to more muted subscriber gains this year: “Netflix will continue to feel the aftereffects of a super-charged 1H20, with a massive pull-forward of demand prompting tempered expectations for 1 million additions in 2Q, its lowest quarterly level since 4Q11. The pull-forward may have also been amplified by price increases and pent-up demand for outdoor entertainment leading to uncertainty in 3Q guidance, though the return of several high-profile titles (‘Witcher,’ ‘Cobra Kai,’ ‘You’ and ‘Money Heist’) will be a clear catalyst for normalizing subscriber gains from 4Q and into 2022.”

LightShed Partners media analyst Rich Greenfield published what he sees as the key questions Netflix investors should ask management after its earnings report. Among them are when Netflix’s subscriber growth will normalize, whether India can be a meaningful driver of profitability, and where the company sees opportunities in video games. Greenfield asks: “Is the goal to leverage IP you create for TV/film or create original video game IP that can be leveraged into TV/film production?”

Another thing to watch out for is how a slowdown in production last year is affecting the service. The filming of new shows and movies basically came to a standstill in early 2020, which curbed output in the following months.

* * *

So with all that in mind, was Q2 the quarter that would finally unleash another repricing higher for Netflix stock? Alas, it would again not be this time because despite beating on the top line, and adding more subscribers than expected, the company missed on EPS and again reported another dismal quarterly guidance which came in well below expectations (full letter to shareholders).

First, the good news:

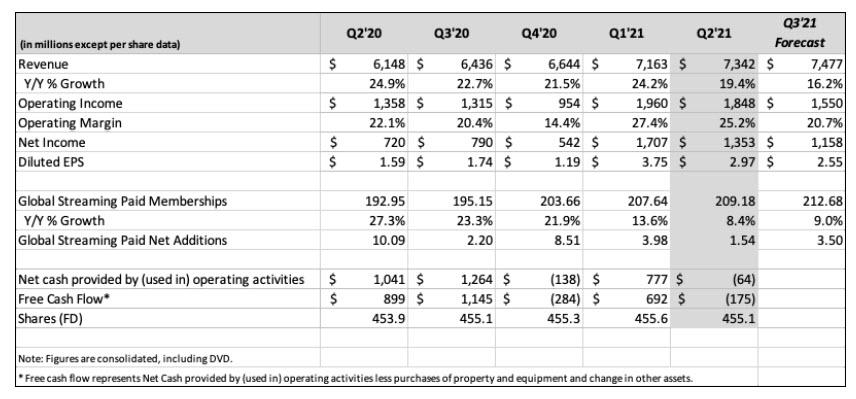

- Q2 revenue $7.34B, beating Est. $7.32B

- Q2 Streaming Paid Net Change +1.54M, beating Est. +1.12M

- Operating margin of 25.2% came in on top of estiamtes of 25.2%

And then the bad news:

- Q2 EPS $2.97 missing consensus Est. $3.14

- Company sees Q3 Streaming Paid Net Change +3.50M, far below the Wall Street estimate of +5.86M

Just as bad, the company reported its first decline in US/Canada paid subscribers, which shrank by 430K to 73.95MM

In other words, while q2 revenue rose 19% and operating income rose 36%, shares tumbled after its third-quarter subscriber forecast missed estimates.

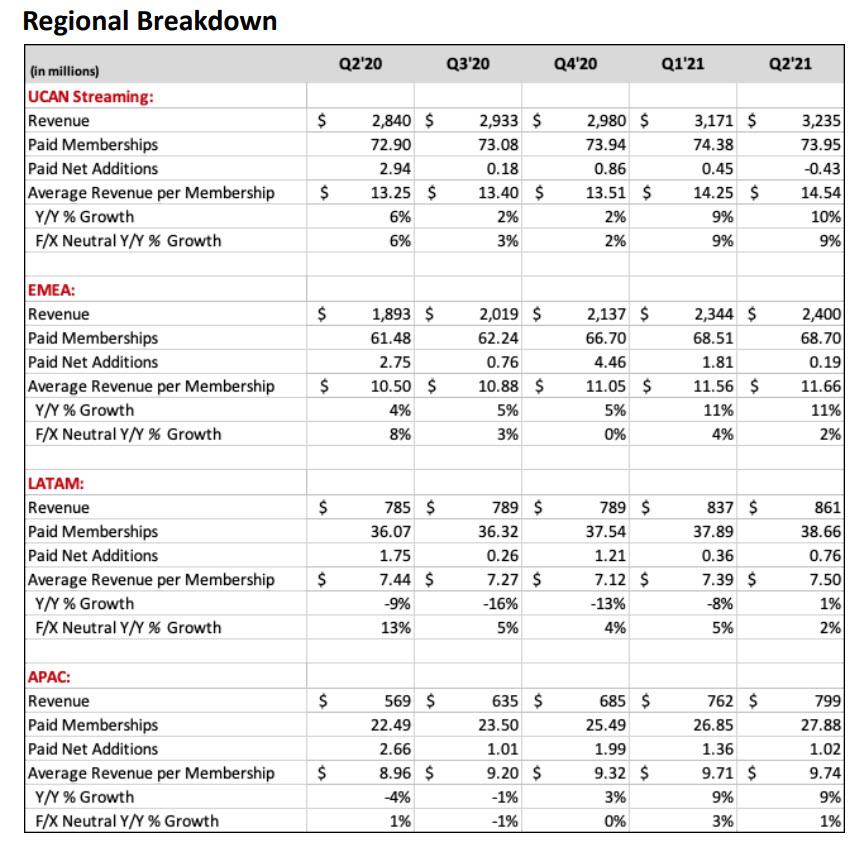

Here is the full breakdown of Q2 subs which saw a drop in US/Canada paid subs:

- UCAN streaming paid net change -430,000, estimate +52,190

- EMEA streaming paid net change +190,000, estimate +429,335

- LATAM streaming paid net change +760,000, estimate +128,719

- APAC streaming paid net change +1.02 million, estimate +524,900

- Total Streaming paid net change +1.54 million, estimate +1.12 million (Bloomberg Consensus)

And visually:

Commenting on the Q2 results, NFLX said that revenue growth was driven by an 11% increase in average paid streaming memberships and 8% growth in average revenue per membership (ARM). “COVID has created some lumpiness in our membership growth (higher growth in 2020, slower growth this year), which is working its way through.”

A more detailed breakdown of why the company continues to see “choppiness” in its earnings:

“The pandemic has created unusual choppiness in our growth and distorts year-over-year comparisons as acquisition and engagement per member household spiked in the early months of COVID. In Q2’21, our engagement per member household was, as expected, down vs. those unprecedented levels but was still up 17% compared with a more comparable Q2’19. Similarly, retention continues to be strong and better than pre-COVID Q2’19 levels, even as average revenue per membership has grown 8% over this two-year period, demonstrating how much our members value Netflix and that as we improve our service we can charge a bit more. “

NFLX also said that it added 1.5m paid memberships in Q2, “slightly ahead of our 1.0m guidance forecast” with the APAC region representing about two-thirds of global paid net adds in the quarter. Meanwhile, as noted above, Q2 paid memberships in the UCAN region were down sequentially (-0.4m paid net adds): “We believe our large membership base in UCAN coupled with a seasonally smaller quarter for acquisition is the main reason for this dynamic. This is similar to what we experienced in Q2’19 when our UCAN paid net adds were -0.1m; since then we’ve added nearly 7.5m paid net adds in UCAN”

This means that the covid pandemic in 2020 pulled forward so many subs that 2021 is shaping up to be the wirst year since at least 2016.

Understandably, now that companies are comping to 2019 not to 2020 (for the dismal base effect), Netflix is urging investors to compare this year to 2019 and not to the same quarter a year ago (when the pandemic boosted subscriber growth). Oddly the company had no problem comparing 2020 to 2019 when the numbers were in its favor, but we digress… The company points out that user engagement per member household was down in the second quarter compared with “those unprecedented levels” of 2020, but it was up 17% “compared with a more comparable Q2’19.”

But while shareholders may excuse the decline in US subs, they were not happy with the company’s overall guidance, where it now sees just 3.5 million new subs in Q3, far below the 5.86 million expected.

* * *

Looking at its content slate, Netflix said it would be light in the first half due to Covid. The company is now playing catch-up, with spending on new TV shows and movies up 41% to $8 billion in the first half. The company is targeting $12 billion in content spending for the year, a 12% bump, to wit:

Through the first half of 2021 we’ve already spent $8 billion in cash on content (up 41% yr-over-yr and 1.4x our content amortization) and we expect content amortization to be around $12 billion for the full year (+12% year over year). Our Q3 slate will include new seasons of fan favorites La Casa de Papel (aka Money Heist), Sex Education, Virgin River and Never Have I Ever as well as live action films including Sweet Girl (starring Jason Momoa), Kissing Booth 3, and Kate (starring Mary Elizabeth Winstead) and the animated feature film Vivo, featuring all-new songs from Lin-Manuel Miranda.

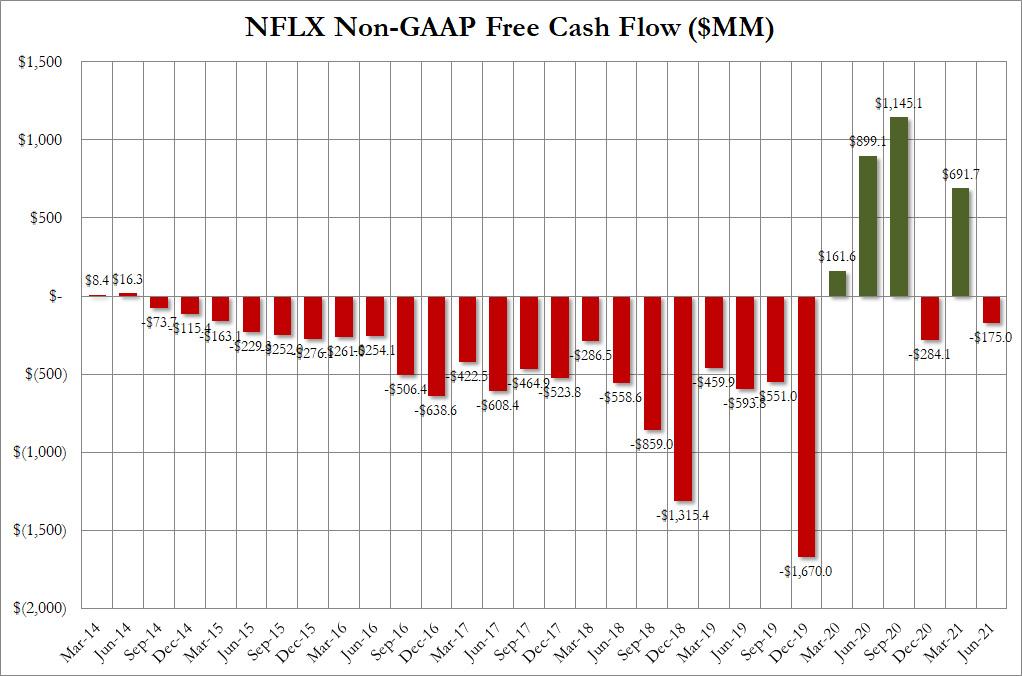

There was more bad news in NFLX cash flow, which after last quarter’s surge reversed again, and dropped by $175 million, vs a positive cash flow of $899 million a year ago. NFLX notes that it is “still expecting full year 2021 free cash flow to be approximately break even.” The company also believes it no longer needs to raise external financing to fund our day-to-day operations. We’ll see if at least that promise pans out.

In other news, during Q2, NFLX increased its revolving credit facility (which remains undrawn) to $1 billion from $750 million and extended the maturity from 2024 to 2026. The company also repurchased 1 million shares for $500 million (at an average per share price of about $500) under our $5 billion share authorization: the company said its “main priority is to invest in the organic growth of our business while maintaining strong liquidity and retaining financial flexibility for strategic investments.”

After all that, the market was unimpressed but it could have been worse: after initially plunging below $500 briefly, the stock has since stabilized down 2% around $515. Among stocks that are down in sympathy, video-streaming platform Roku falls 1.4%.

developing

Tyler Durden

Tue, 07/20/2021 – 16:16

Continue reading at ZeroHedge.com, Click Here.