Feature your business, services, products, events & news. Submit Website.

Breaking Top Featured Content:

“Clampdown”: Watch Gundlach’s Latest Webcast Live

It’s that time of the month when Bond King Jeff Gundlach regales his subjects, and investors in his DoubleLine, with his latest monthly thoughts revealed in the periodic webcast for this Total Return Fund.

Since it’s been about three months since Gundlach’s March 9 webcast when he laid out his outlook for the year, here is a recap of what he said then courtesy of Bloomberg:

- Gundlach reiterated his bearish dollar call in the short-term, saying the greenback will be correlated to the budget. The Bloomberg Dollar Index has since declined 2.4% since he said that.

- He called the Nasdaq “dicey,” making a daring call that it could eventually drop as much as it did from 2000 to 2003 (after the dot-com bubble deflated.) He also said it was unlikely to outperform, which he ended up being right about. Since those comments, the Nasdaq Composite rallied 6% relative to the S&P 500’s 9% gain.

- He called for a modest or moderate decline for long bond yields, but held his call for the 10-year yield eventually hitting 3%. Since then, the 10-year yield has remained unchanged, but the yield on the 30-year declined by two basis points.

Bottom line, as Bloomberg grundglingly admits, “in the last three months, his call on the Nasdaq, dollar and long bond yields have all been correct.”

Looking ahead, fans of Gundlach will be curious to hear his updated thoughts on inflation and the stock market. In April, Gundlach said it wasn’t clear that U.S. inflation will be “transitory,” as Federal Reserve economists have been trying to convey this year (and as Deutsche Bank dramatically posited this week). “How do they know that when there’s plenty of money printing that’s been going on and we’ve seen commodity prices going up really massively,” he told BNN Bloomberg at the time.

Gundlach also added that the U.S. stock market was overvalued by virtually every important metric versus foreign markets such as those in Asia and Europe. He disclosed that he’d bought European stocks “literally for the first time in many years. I can’t remember the last time I did it. And that’s largely because I think the U.S. dollar is almost certain to decline over the intermediate to long term.”

With the Stoxx 600 trading at a record high, this was yet another correct call.

Focusing on the economy, in his last call Gundlach put an emphasis on the jobs market, where only idiots and Fed employees don’t realize that we are facing a historic crisis due to labor shortages resulting from Biden’s massive handouts. Gundlach is likely to comment on the last two payrolls reports, both of which were major disappointments. This will likely be key to his arguments on where markets are going next because he likes to dive into savings, income and spending trends, all of which are tied to the labor market.

With that in mind, here is Gundlach’s latest webcast “Clampdown” – click on the image below to get to the webcast page (registration required). Why the title? Because to Gundlach “clampdown” is another term for the continuing lockdowns the bond king is seeing in California.

In his presentation, Gundlach starts off by talking about the soaring US GDP and budget deficit, and points out that the enabler of it all is the Fed and its balance sheet which at last check was just under $8 trillion.

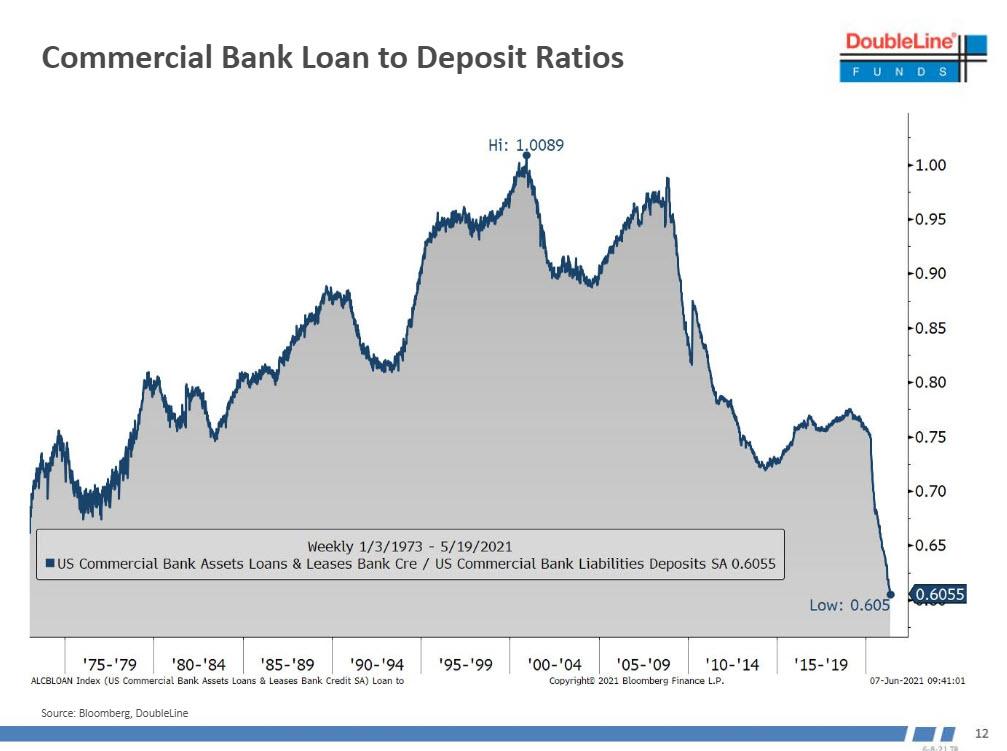

Gundlach then discusses the topic of our April post pointing out the “stunning divergence” between soaring bank deposits (which banks may soon start charging money on, i.e., negative deposit rates) and shrinking bank loans (spoiler alert: the Fed is also responsible for this as we explained).

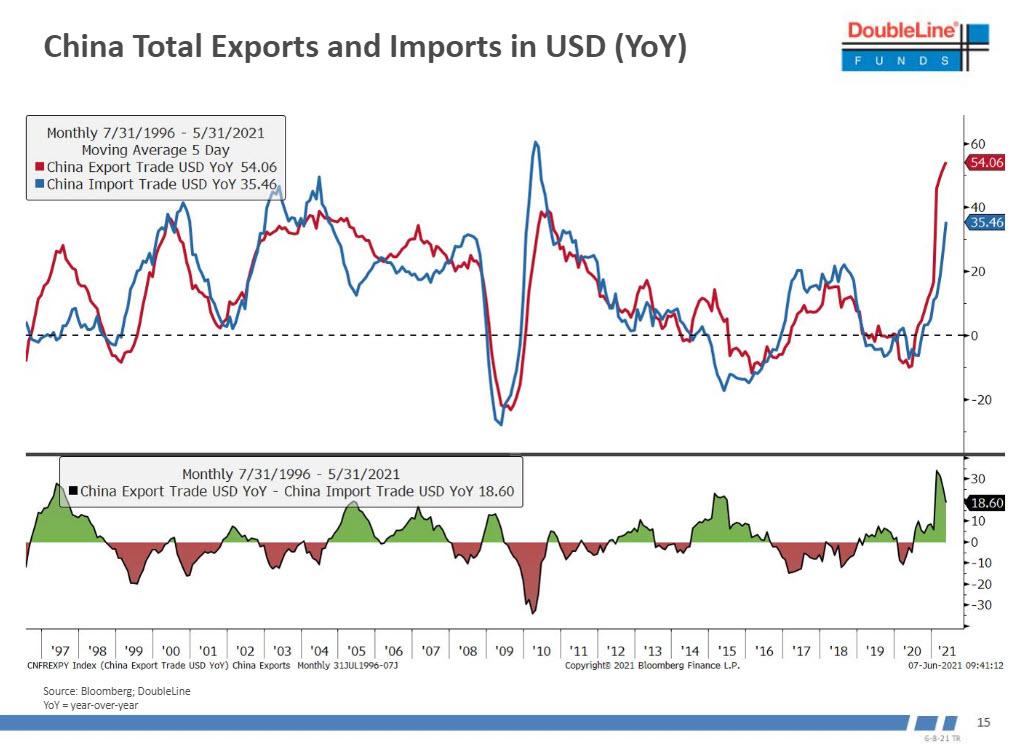

Gundlach then takes a quick look at the soaring gap between Chinese import and export growth, and points out that the spread is now the widest it has been since 1997. “We’ve really been helping out the Chinese economy,” Gundlach says. A lot of U.S. spending, held up by government assistance, is going on goods from China and Southeast Asia.

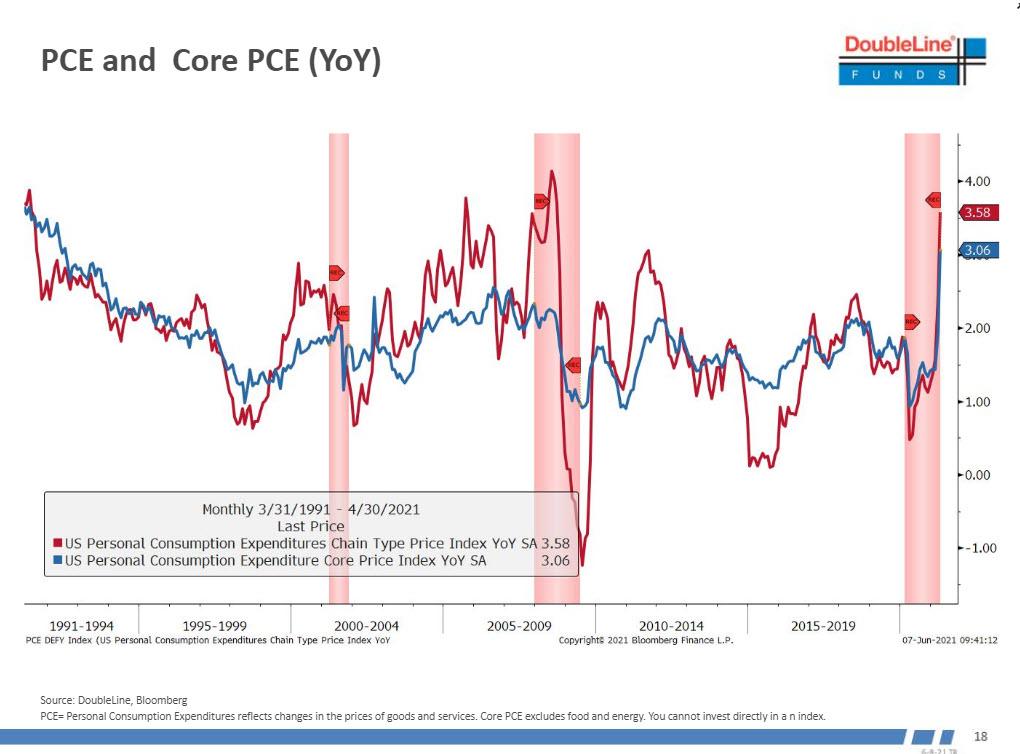

Gundlach then shifts to inflation, and points out that both core PCE and CPI are showing 3%+ prints (we’re at 3.58% in PCE and above 3% in core PCE, which we haven’t seen since the 1990s). This is in the context of the “transitory” discussion, where Gundlach says “How could i know” when asked rhetorically if inflation will be transitory or permanent. He does ask, however, how much resolve will the Fed have on not tapering if there is a 5% print. Gundlach also said one thing that’s troubling about the transitory inflation narrative is if you have to pay more now than in the future, which could be a fallout of the government response.

Tyler Durden

Tue, 06/08/2021 – 16:21

Continue reading at ZeroHedge.com, Click Here.